2020-05-05 09:31:00 Tue ET

stock market technology facebook covid-19 apple microsoft google amazon data platform network scale lean startup artificial intelligence antitrust alpha patent model tech titan unicorn tesla global macro outlook

Our fintech finbuzz analytic report shines fresh light on the fundamental prospects of U.S. tech titans Facebook, Apple, Microsoft, Google, and Amazon (F.A.M.G.A.). As of Spring-Summer 2020, this analytic report focuses on the competitive advantages, opportunities, and threats for F.A.M.G.A. in the modern age of digital tech diffusion. Key opportunities arise in the broad context of social media, consumer technology, software, Internet search, e-commerce, and cloud service provision etc. In contrast, the primary threat is closer antitrust scrutiny on the sheer size, power, and product market dominance of F.A.M.G.A. as many U.S. institutions mistrust tech titans in American history. Our fundamental analysis focuses on the key actionable insights and metrics for the corporate performance and stock valuation of each tech titan. Our quantitative analysis accords with the standard approach to discounting-cash-flows (DCF) corporation valuation.

We provide a soft PDF version of this analytic report in the cloud: https://bit.ly/2VzRnjD

This analytic report cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, and other financial issues. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

U.S. tech titans Facebook, Apple, Microsoft, Google, and Amazon (FAMGA) enjoy a stock market bull run in recent times even as global regulators probe into antitrust issues and activists fret about consumer privacy problems. The sharp rise of stock market capitalization for these American tech titans is about $2 trillion or equivalent to the German stock market valuation. At least 4 out of these 5 primary tech giants, Alphabet, Amazon, Apple, and Microsoft are each worth more than $1 trillion, and Facebook is worth $620 billion. Despite the current techlash in Silicon Valley, New York, and Seattle etc, most fund managers worldwide have chosen to move onto the next stage of high-tech stock investment valuation. This calculus suggests that these U.S. tech titans continue to operate as core platform enterprises with positive network effects, scale economies, and information cascades. Competitive moats and first-mover advantages empower these open platform enterprises to earn new riches amid economic policy uncertainty around the current corona virus pandemic outbreak in 2020.

The recent surge in high-tech stock market valuation raises at least 2 major worries. First, institutional investors and retail traders may or may not prevent a speculative asset bubble in the big tech sector. The 5 major tech giants account for $4.6 trillion stock market capitalization or 20% of the S&P 500 stock market index. In fact, the millennium dotcom bubble serves as a precedent in American stock market history and eventually triggers a financial market downturn at the start of the new century. Second, the opposite investor concern is that the current tech stock valuation may turn out to be right. The recent $2 trillion big tech bull run suggests that high-tech profits are likely to double or so in the next decade. This bullish investor sentiment may extrapolate in to the foreseeable future. The inadvertent ramifications can be economic tremors in rich countries with an unfair distribution and concentration of both socio-economic market power and political clout.

In recent years, the 5 U.S. top tech titans crank out almost $200 billion annual cash flows after capital investments. In stark contrast, the loss-laden antics of flaky tech unicorns such as Lyft, Netflix, Uber, WeWork, and Zoom etc may evoke some sort of speculative froth toward the tail end of a long-term tech boom. Global regulators can punish many tech firms for tax evasion, privacy intrusion, and anti-competitive misconduct. However, their regulatory fines and penalties amount to less than 1% of the stock market valuation of Facebook, Apple, Microsoft, Google, and Amazon (FAMGA). After all, such punitive fines and penalties seem to be tolerable costs of operating open platform enterprises in social media, mobile connectivity, software, Internet search, e-commerce, cloud service provision, and so forth. In most OECD countries, only 10% of retail sales are online via Alibaba, Amazon, and eBay, and perhaps 20% of computer workloads land in the cloud with Amazon, Microsoft, and Google etc. FAMGA can often operate beyond national boundaries, and this global reach allows big tech to expand at an exponential pace. Digital technology diffusion remains relatively low in non-OECD countries in key comparison to ubiquitous and pervasive big tech adoption in most OECD countries. In this positive light, FAMGA can continue to boost their global user growth and monetization in the next decade.

Nowadays, FAMGA employ more than 1 million people and spend $200 billion per year in Corporate America. The less rosy picture outside the U.S. seems to be a tumult of regulatory experiments. China now keeps its Internet titans such as Baidu, Alibaba, and Tencent under tacit state control and then wants to rely less on Silicon Valley (i.e. FAMGA and several other tech unicorns). At least 27 countries such as Australia, Brazil, France, Germany, and Indonesia consider imposing digital taxes on FAMGA for jurisdictional reasons. Also, India forcefully regulates e-commerce and online speech. Moreover, the European Union wants individual users to own-and-control their personal data. E.U. General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA) are good examples of current checks and balances for global regulators to safeguard against FAMGA market power and dominance. In essence, the law of inadvertent consequences counsels caution.

Digital data are not mere mathematical representations of real ones. In fact, digital data help strengthen the adage that knowledge is power. Digital data help optimize many practical applications from headset acoustics to national transport networks. Digital data enable all sorts of artificial intelligence algorithms to recognize objects and faces. Also, these artificial intelligence algorithms help many economic agents and other end users distinguish voices, speeches, and smells. Digital data agents analyze specific complex human decisions and patterns in the broader context of new business models.

The new data economy grows fast in terms of the exponential pace of digital data growth. A genetic research firm 23andMe acquires more than 10 million customers, and each of these customers provides his or her unique human genome sequence of 3 gigabytes of data. One of the big 4 banks analyzes almost 3 petabytes of retail consumer data for retail risk capital quantification for mortgage loans, credit cards, auto loans, specialty loans, and small business retail loans. The new autonomous vehicles produce almost 30 terabytes for every 8 hours of real-world transport on the road. A global market research firm IDC expects the modern world to generate 90 zettabytes of data per year from 2020 to 2025. This exponential data generation exceeds the vast amount of electronic data since the advent of personal computers.

However, this rapid digital data growth poses tensions and trade-offs too. In some ways, digital data lakes serve as metaphorically natural resources such as oil, air, and water. People can choose to own these digital data lakes; and others can trade data for profits and other non-cash rewards. For instance, financial media sources such as Bloomberg, CNBC, and Economist etc spend millions of dollars each year to purchase real-time global economic data from third-party service providers such as IEX and Nasdaq. Digital data also show characteristics of most public goods as these public goods help maximize wealth creation through their ubiquitous usage. New legal rules and institutions should help regulate these tensions and trade-offs for better intellectual property protection.

Many companies intend to use digital data to infuse their corporate decisions and applications with artificial intelligence. Many data scientists, econometricians, and machine-learning experts can help delve into data lakes or central repositories for extracting useful business insights that shine new light on core corporate decisions. At the same time, several governments start to assert their digital sovereignty to require that some sensitive digital data cannot leave their country of origin. Due to jurisdictional state control, these governments strive to preserve personal privacy as tech titans, tech unicorns, and other lean enterprises continue to mine valuable data for premier consumer analytics. In turn, these consumer analytics help inform how tech titans and lean startups can connect their core products and services to their target audiences. In essence, such global connections and numerous iterative continuous improvements help reach a viable product-market fit in the long run. In time, these tech bellwethers can scale this exponential product-market fit for more efficient customer acquisitions.

To the extent that many tech titans and lean startups successfully transform digital data lakes into new and useful business insights and consumer analytics, this dual transformation poses the risk of unequal income and wealth distribution. As digital data become major competitive moats and first-mover advantages, tech titans and unicorns monetize these data-driven moats and advantages. Specifically, Google and Facebook extract substantial economic rent from online ads; Amazon, Alibaba, Google, and Microsoft earn regular fees and surcharges from their cloud software service provision; and Apple, Google, and Microsoft leverage mobile connectivity and software usage to reap substantive net profits at near-zero marginal costs. In this digital economy, tech titans tend to become the big beneficiaries of data-driven business insights and consumer analytics. In this fresh light, governments need to reconsider the public policy implications for tax avoidance, privacy protection, and antitrust scrutiny. Digital plurality continues to push the boundaries for these public policy issues. On balance, both tech corporations and regulatory agencies should strike a delicate balance between these tensions and trade-offs in the modern data economy. Whether global regulators should treat tech titans as utility corporations (such as telecoms and electric service providers) remains an open controversy.

Many metaphors can describe data flows. Some economists liken data to oil in the sense that data flows are the fuel of the future for modern tech titans and unicorns. In recent times, the comparison has been with sunlight because data can soon be like solar rays everywhere. Several other economic media commentators also talk of data as infrastructure. In this alternative interpretation, data can be viewed as a kind of digital twin of roads or railways. In this way, data require public investments and new rules and institutions for better long-term management.

This multiplication of metaphors reflects the malleable economic treatment of data. First, data are non-rivalrous because their digital copies can be infinite. This non-rivalry suggests that many people can use the same data without limiting their use by others. Second, data are also excludable because new tech advances such as encryption can control who has access to data. Core responsible parties determine where one sets the cryptographic slider. In light of these considerations, data can be private goods like oil or public goods like sunlight. Alternatively, data can serve as new tech club goods between private goods and public goods due to non-rivalry and excludability.

Online advertisement may be the largest marketplace for personal data. Numerous Internet advertisers buy clicks, page views, and impressions on the basis of a close digital profile of each online viewer. The online ad market value is near $200 billion as of early-2020. Also, online data brokers track thousands of data points for each online viewer and further sell these data to banks, telecoms, pharmaceutical firms, insurance companies, and so forth. The annual revenue can exceed $20 billion for this Internet data exchange worldwide.

Moreover, it can be profitable for data scientists, econometricians, and statisticians etc to analyze data flows in order to offer business insights. For instance, Google sponsors Kaggle as an online series of machine-learning contests, and thousands of teams of data scientists and econometricians now compete against one another to design the best algorithms for predicting energy consumption, video authenticity, or the likely transmission of Covid-19 or corona virus pandemic outbreak in 2020. Facebook, Apple, Microsoft, Google, and Amazon (FAMGA) rarely ever sell data; but these tech titans sell business insights into the best target audiences for online ads. In this unique fashion, most tech titans extract hefty economic rent from digital ad channels more efficiently than the traditional counterparts such as TV and radio.

Nowadays, it is difficult to delineate personal data as some form of property rights. An Internet search engine (Google or Microsoft Bing), a social network (Facebook or Twitter), or an e-commerce platform (Amazon or eBay) can make quite accurate predictions about each online viewer by crunching data from many other users with no additional purchases of personal data. Several cloud software service providers from Amazon and Microsoft to Alibaba, Google, IBM, and Oracle etc now operate online marketplaces for smooth bilateral data flows. Like an online store for smart phone apps, these online marketplaces empower users to subscribe to data feeds under specific terms and conditions. These subscriptions serve as the licenses for key users to hunt for data within the digital space. Cloud software service providers such as Amazon Web Services (AWS) and Microsoft Azure receive regular fees in exchange for this cloud software service provision.

As the oil metaphor can be viewed as increasingly problematic, the comparison of data to sunlight, air, and water has risen in flavor. This latter alternative metaphor suggests that we must use data insights as much as possible in order to maximize social welfare. For this reason, many proponents support the open-data movement. Its champions encourage organizations, governments, and universities etc to give away their data such that several other teams such as tech titans and lean startups can use the data for broader practical applications in Internet search, social media, software, mobile connectivity, e-commerce, cloud service provision, and so forth.

However, open data can go only so far when the data-as-sunlight analogy breaks down in practice. For personal data, the main limitations include increasingly strict privacy laws and regulations such as the E.U. General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA). For corporate data, the checks and balances are economic in nature as firm-specific data generation can be prohibitively expensive. Sometimes key data may inadvertently reveal too much about the inventive elements and features of major business products and services. This logic suggests that lean enterprises must make strategic decisions about what data should be open to the global general public.

Data stewardship takes different forms worldwide. In America, data can be viewed as oil, natural gas, or many other private goods: whoever extracts data owns them. In China, data are more like public goods since the government retains the ultimate control and ownership of data (although there are also data-driven online platforms such as Alibaba, Baidu, Tencent, TikTok, and WeChat etc). In Europe, regulators tend to see data as infrastructure. The European Commission plans to support the creation of public data trusts for health care, higher education, residential property protection, and other resource allocation. In a nutshell, all these data trusts, checks, and balances help ensure sound governance mechanisms for better data integrity and privacy protection. Strategic considerations precede ubiquitous and pervasive open data usage and provision.

As of mid-April 2020, U.S. Defense Department inspectors find that the $10 billion JEDI cloud contract with Microsoft seems to be free from any political influence by the White house. However, Defense Department inspectors note in a special report that they cannot complete a fair and reasonable assessment of key allegations of ethical misconduct because the White House offers minimal cooperation.

The new 313-page report summarizes key conclusions from a regulatory review of the Joint Enterprise Defense Infrastructure (JEDI) cloud-computing contract done by the Defense Department Office of Inspector General. This cloud contract seeks to modernize IT operations at the Pentagon. Over as many as 10+ years, this JEDI cloud contract can be worth almost $10 billion.

Microsoft first received the $10 billion cloud contract in October 2019. In November 2019, Amazon Web Services (AWS) filed a landmark lawsuit in the U.S. Court of Federal Claims to protest the controversial JEDI decision. Amazon pointed out that the Trump administration might bias against Amazon and its CEO, co-founder, and chairman Jeff Bezos as the Pentagon granted the JEDI cloud contract to Microsoft.

The JEDI cloud contract draws much scrutiny because this exclusive deal involves President Trump as he often criticizes Amazon and Bezos. The Trump team might spin the JEDI cloud contract because a recent book on the then-Defense Secretary James Mattis suggests that President Trump might have prodded Mattis to exclude Amazon out of the JEDI cloud contract.

There is no substantive evidence that the White House or any other senior people exert pressure on the JEDI contract evaluation and award process. Department of Defense spokesperson Robert Carver states that the inspector report confirms the fair integrity of Pentagon JEDI cloud procurement in accordance with the law. This report should finally close the door on the media and corporate attacks on the core career procurement bureaucrats who have been working tirelessly together to get the essential cloud-computing environment into the hands of frontline warfighters (as the relevant technocrats continue to protect American taxpayers).

Microsoft corporate vice president of external communications, Frank Shaw, states that the official inspector report confirms fair and proper JEDI procurement by the Department of Defense. Amazon might bid too high a price in the first place. Both Amazon and Microsoft retain their own proprietary information about affordable bid prices. At this stage, Amazon appears to delay critical work on cloud infrastructure for national defense. Meanwhile, it is difficult to definitively determine the full extent and nature of key interactions between the Trump team and senior bureaucrats at the Department of Defense in regard to the JEDI cloud procurement process. After the dust settles on JEDI cloud procurement, the law of inadvertent consequences counsels caution.

At this stage, it is quite unlikely for the Trump administration and other White House bureaucrats to interfere with the current JEDI cloud procurement process despite some opposite allegations from the media and some parts of Corporate America. These unfair allegations seem to skew the (counter)arguments in favor of Amazon and Bezos, whereas, Microsoft continues to retain its competitive moats in building Defense Department cloud software service infrastructure.

In the meantime, Amazon dominates in cloud service provision in the private sector; whereas, Microsoft now stands on its feet in the public-sector counterpart. Whether these dominant cloud service providers enter the uncharted territory of each other remains an open controversy. In the next 2 to 5 years or so, Amazon and Microsoft continue to be the formidable duo in U.S. cloud software service provision.

In light of this contentious JEDI cloud procurement and award evaluation process, Amazon Web Services (AWS) and Microsoft Azure may emerge as the cloud duo across the competitive industry landscape. In terms of market penetration, the next cloud service providers are Google, Alibaba, IBM, Oracle, Salesforce, Rackspace, SAP, and VMWare. Cloud software service provision often reaps 70%-90% gross margins and 50%-60% net profit margins. These hefty gains far exceed the thinner 10%-15% gross margins and 3%-5% net profit margins for the current retail sector (and even e-commerce). In the next decade or so, Amazon and Microsoft tend to compete ferociously as a typical duopoly in the cloud software service sector. The other cloud market players can gradually pick up residual market share penetration both in the U.S. and non-U.S. markets.

The number of smart mobile devices will likely reach 25 billion by 2025. This sharp explosion is the natural outcome of a structural shift in big data collection. The next generation of mobile technology, 5G, supports at least 1 million mobile connections per square kilometer. Mobile networks can carry 160 exabytes of global data each month by 2025. This data workload quadruples the current amount.

More data flow into the cloud-computing factories by Amazon Web Services (AWS), Microsoft Azure, Alibaba Cloud, and Google Cloud etc. In most cases, these cloud software service providers offer high-performance computer power for global users to train smart machine-learning algorithms that help quickly detect credit card fraud, automatic machinery for maintenance, or smart encryption for mobile data storage. AWS and Microsoft Azure etc strive mightily to deepen data centralization. These cloud software service providers offer end users cost-effective software that helps manage mobile devices. Specifically, AWS and Azure provide at least 14 ways to transfer data into the cloud. These feasible ways include several software services via the Internet and offline methods such as cloud lorries with digital data storage of up to 100 petabytes.

The universal law of data gravity suggests that most companies move more of their business applications to the cloud-computing skies once these companies put their important data in the cloud. As a result, this greater data storage allows most cloud service providers to extract even more revenue. These cloud service providers can further offer an increasingly rich palette of services that empower cloud customers to mine their data for better business insights.

At some stage, global users need to aggregate data together such that these users can train econometric machine-learning models and algorithms to extract business insights. In turn, these insights help inform good and pragmatic corporate decisions. From a fundamental perspective, many artificial intelligence experts expect cloud-computing nodes to be more equally spread between the cloud and its edge. Most data scientists, econometricians, and statisticians need to train quantitative models and algorithms centrally in the cloud when substantial data flows originate from the edge. Given the right incentives, big cloud software service providers may face the temptation to analyze data on the fly somewhere between the cloud center and its edge. If the world has to refrain from drowning in the digital data ocean, it may be opportune for governments and regulators to reconsider taxing big data generation in the cloud.

Since data often no longer manifest in the form of static blocks, but rather real-time digital data feeds and flows, it is important for cloud software service providers and end users to treat these new data streams as different data sources. New artificial intelligence assembly lines serve as cloud-computing tools for data scientists and econometricians to train quantitative models and algorithms for specific continuous business applications. These applications encompass health care, electric power generation, higher education, residential real estate management, trademark and patent protection, financial risk analysis, and relational database management etc. As the global workhorse vendor of corporate IT relational databases, Oracle aims to entrench its current dominance by providing autonomous databases. This cloud data service combines and automates all kinds of digital repositories with artificial intelligence applications so that business clients need not have to pull together all these cloud computer programs on a standalone basis. Such data integration can be essential to boosting firm-specific data productivity in terms of the dollar output per data input.

As an online service for customer relationship management, Salesforce has spent billions in recent years to develop its own artificial intelligence technology, Einstein, with 2 recent major acquisitions of big-data companies MuleSoft and Tableau. As Salesforce president and chief operating officer Bret Taylor suggests, the prescient business goal is to empower firms to consolidate their customer data. In this unique fashion, these firms can focus on a single holistic view of their customers, so it can become easier for firms to analyze the up-to-date customer profiles, relations, and strategies. This fundamental analysis helps personalize fresh offers, products, and services to the best target audiences. Several other smaller lean startups such as Databricks, Qlik, and C3.ai provide similar transformative analytics for better data visualization and mobile platform usage.

In recent years, many countries erect virtual borders in the digital cloud. The E.U. General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA) allow personal data to leave Europe and America respectively only if firms have appropriate safeguards in place or if the destination country has an adequate level of data protection. India blocks credit card and other electronic payment data from leaving the country and may soon require that specific types of personal data can never leave the country. Russia insists and requires that only domestic servers can process data within its territory. China blocks most international data flows. In practice, many other countries seek to establish jurisdictional laws and regulations to prohibit tax avoidance, privacy intrusion, and anti-competitive misconduct.

On the one hand, it can be both tricky and expensive to build a domestic cloud for each country. On the other hand, an excessively protectionist country may witness an exodus of cloud software service providers that refuse to serve the small market. On balance, different data coalitions have begun to form in practice. The U.S. has started a virtual data club with the Cloud Act 2018 to empower the government to negotiate reciprocity agreements with other countries. If these countries allow U.S. law enforcement to access data in some partner territory, these non-U.S. countries can get easier reciprocal access to data found in the American territory. Britain has already signed this U.S. Cloud Act reciprocity agreement; and the European Union expects to do so soon. In a nutshell, these digital data coalitions go beyond national boundaries and can serve as the strategic solution to the paradox of non-rivalrous and exclusive club goods for the modern data economy.

The modern data economy poses economic inequality as a potential threat to the wealth of nations. A few platform orchestrators such as Facebook, Apple, Microsoft, Google, and Amazon (FAMGA) dominate the modern data economy. In early-2020, FAMGA receive a joint net profit of about $55 billion, which is an order of magnitude more than the joint net profit of the next 5 most valuable American tech firms from 2015 to 2020. This corporate inequality arises from positive network effects, scale economies, competitive moats, first-mover advantages, and information cascades. Size begets size. These top tech titans can afford to recruit the best data scientists and econometricians etc and further have the cash to buy the best lean startups in artificial intelligence, smart data analysis, and relational database management etc.

China and America now account for 90%+ of the stock market capitalization of the 70 largest digital platforms worldwide (in stark contrast to only 1% for Latin America and Africa). The top-notch U.S. digital platform include Facebook, Apple, Microsoft, Google, and Amazon (FAMGA) as well as several other lean enterprises such as Airbnb, Netflix, Oracle, PayPal, Salesforce, Twitter, and Uber etc. Furthermore, the Chinese platform orchestrators include Baidu, Alibaba, and Tencent (BAT) as well as JD.com, Meituan, Pinduoduo, TikTok, and Zoom. Several economists now warn that both the Chinese and American economies risk becoming mere data providers while the top tech titans there need to pay for the digital data collection and artificial intelligence in the virtual data economy.

The unequal distribution of both income and wealth between capital and labor may turn out to be the most serious problem of the virtual data economy. As this virtual data economy grows, more high-skill labor tends to migrate to China and America. The next global techlash may inadvertently emerge from the collective wisdom of both human comprehension and artificial intelligence. Global tech titans and digital platform orchestrators such as FAMGA and BAT are not only monopolies but also monopsonies: these tech giants have substantial labor market power to hold down wages for data workers. In reality, these top tech titans and other lean enterprises can refuse to pay hefty prices for user data if these high-tech corporations manage to infer specific end user data from some other sources in more cost-effective ways. For instance, tech-savvy econometricians and machine-learning experts can often manage to extract individual DNA from the broader genetic databases of his or her family members. At this stage, no government imposes taxes on these digital data dividends. In summary, it is important for global regulators to enforce new effective rules and institutions to deter tax avoidance, privacy intrusion, and anti-competitive misconduct in at least most OECD countries.

Due to the recent rampant corona virus pandemic outbreak worldwide, we should refrain from presenting the keystone stock investment thesis and market valuation for each of the 5 U.S. tech titans Facebook, Apple, Microsoft, Google, and Amazon (FAMGA). Discounting-cash-flows (DCF) and free-cash-flows (FCF) stock market valuation methods may or may not lead to reasonable ranges of target share prices for these high-tech corporations amid substantial economic policy uncertainty and subsequent coronavirus transmission. Our previous FAMGA stock valuation report delves into the quantitative details of both DCF and FCF fundamental analysis for each of the 5 U.S. tech titans as of Fall-Winter 2019.

During this interim period, we have chosen to defer this algorithmic quantification of both DCF and FCF target share prices until the dust settles on the global corona virus outbreak. At this stage, we hope to resume our core quantitative fundamental analysis of each of the 5 U.S. top tech titans FAMGA with relevant benchmarks in the foreseeable future. In the new normal state of global economic affairs, we can better manage to analyze relevant and reasonable ranges of target share prices for FAMGA in terms of their fundamental characteristics such as positive network effects, scale economies, first-mover advantages, information cascades, and other competitive moats etc.

As of mid-2020, we list our proprietary dynamic conditional alphas for the U.S. top tech titans Facebook, Apple, Microsoft, Google, and Amazon (FAMGA). Our core proprietary alpha stock signals enable both institutional investors and retail traders to better balance their key stock portfolios. This delicate balance helps gauge each alpha, or the supernormal excess stock return to the smart beta stock investment portfolio strategy. This proprietary strategy minimizes beta exposure to size, value, momentum, asset growth, cash operating profitability, and the market risk premium. Our unique proprietary algorithmic system for asset return prediction relies on U.S. trademark and patent protection and enforcement.

Our proprietary alpha stock investment model outperforms the major stock market benchmarks such as S&P 500, MSCI, Dow Jones, and Nasdaq. We implement our proprietary alpha investment model for U.S. stock signals. A comprehensive model description is available on our AYA fintech network platform. Our U.S. Patent and Trademark Office (USPTO) patent publication is available on the World Intellectual Property Office (WIPO) official website.

Our core proprietary algorithmic alpha stock investment model estimates long-term abnormal returns for U.S. individual stocks and then ranks these individual stocks in accordance with their dynamic conditional alphas. Most virtual members follow these dynamic conditional alphas or proprietary stock signals to trade U.S. stocks on our AYA fintech network platform. For the recent period from February 2017 to February 2020, our algorithmic alpha stock investment model outperforms the vast majority of global stock market benchmarks such as S&P 500, MSCI USA, MSCI Europe, MSCI World, Dow Jones, and Nasdaq etc.

Do you find it difficult to beat the long-term average 11% stock market return?

It took us 20+ years to design a new profitable algorithmic asset investment model and its attendant proprietary software technology with fintech patent protection in 2+ years. AYA fintech network platform serves as everyone’s first aid for his or her personal stock investment portfolio. Our proprietary software technology allows each investor to leverage fintech intelligence and information without exorbitant time commitment. Our dynamic conditional alpha analysis boosts the typical win rate from 70% to 90%+.

Our new alpha model empowers members to be a wiser stock market investor with profitable alpha signals! The proprietary quantitative analysis applies the collective wisdom of Warren Buffett, George Soros, Carl Icahn, Mark Cuban, Tony Robbins, and Nobel Laureates in finance such as Robert Engle, Eugene Fama, Lars Hansen, Robert Lucas, Robert Merton, Edward Prescott, Thomas Sargent, William Sharpe, Robert Shiller, and Christopher Sims.

Follow AYA Analytica financial health memo (FHM) podcast channel on YouTube: https://www.youtube.com/channel/UCvntmnacYyCmVyQ-c_qjyyQ

Follow our Brass Ring Facebook to learn more about the latest financial news and fantastic stock investment ideas: http://www.facebook.com/brassring2013.

Free signup for stock signals: https://ayafintech.network

Mission on profitable signals: https://ayafintech.network/mission.php

Model technical descriptions: https://ayafintech.network/model.php

Blog on stock alpha signals: https://ayafintech.network/blog.php

Freemium base pricing plans: https://ayafintech.network/freemium.php

Signup for periodic updates: https://ayafintech.network/signup.php

Login for freemium benefits: https://ayafintech.network/login.php

We update and refresh part of memetic financial information on a sporadic basis. We aim to facilitate this information exchange only for illustrative purposes. Some information may be stale and incomplete. Therefore, we recommend each member to consult the respective external website(s) for more up-to-date information.

This analytic report cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, and other financial issues. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

The conventional disclaimers apply to this key case where each freemium member bewares, understands, and acknowledges the service terms and conditions for our courteous fintech network platform. Any omissions, errors, or other blemishes do not necessarily reflect the official views and opinions of our AYA fintech platform orchestrator. We make a conscious effort to keep most major omissions to 1% to 5% of the fintech information for about 6,000 U.S. stocks on NYSE, NASDAQ, and AMEX. These omissions tend to concentrate around some rare corporate events (e.g. IPO, delisting occurrence and recurrence, abrupt trading suspension, and M&A initiation etc). Overall, these disclaimers, terms, and conditions of our service should be viewed as baseline house rules for fintech network platform usage and development.

Under pending subsequent patent-law confirmation, the relevant legal text protects our proprietary alpha software technology for ubiquitous knowledge transfer. Each freemium member enjoys his or her interactive usage and information exchange on our AYA algorithmic fintech network platform with sound and efficient dynamic conditional asset return prediction.

Our AYA fintech network platform helps promote better financial literacy, inclusion, and freedom of the global general public with an abiding interest in core economic reforms, financial markets, and stock market investments. In this broader context, each freemium member can consult our mission statement that provides more in-depth explanatory details on our long-term aspiration.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2023-10-28 12:29:00 Saturday ET

Paul Morland suggests that demographic changes lead to modern economic growth in the current world. Paul Morland (2019) The human tide: how

2020-11-22 11:30:00 Sunday ET

A brief biography of Andy Yeh Andy Yeh is responsible for ensuring maximum sustainable member growth within the Andy Yeh Alpha (AYA) fintech network pla

2019-02-25 12:41:00 Monday ET

Chicago financial economist Raghuram Rajan views communities as the third pillar of liberal democracy in addition to open markets and states. Rajan suggests

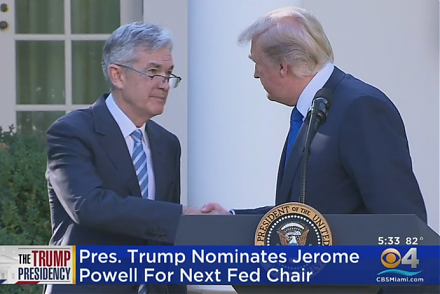

2017-10-03 18:39:00 Tuesday ET

President Trump has nominated Jerome Powell to run the Federal Reserve once Fed Chair Janet Yellen's current term expires in February 2018. Trump's

2019-07-21 09:37:00 Sunday ET

Facebook introduces a new cryptocurrency Libra as a fresh medium of exchange for e-commerce. Libra will be available to all the 2 billion active users on Fa

2023-06-14 10:26:00 Wednesday ET

Daron Acemoglu and James Robinson show that good inclusive institutions contribute to better long-run economic growth. Daron Acemoglu and James Robinson