Brass Ring International Density Enterprise (BRIDE)

Our proprietary alpha model for asset management draws from the recent U.S. software utility patent submission, "Algorithmic system for dynamic conditional asset-pricing analysis and financial intelligence technology platform automation" (USPTO #15/480,765 as of Thursday 4 April 2017). This key software invention relates to the new, non-obvious, and applicable macroeconometric design and implementation of an algorithmic system for better risky asset return prediction and fintech network platform automation. The critical elements of new software technicality pertain to our dynamic conditional estimation of fundamental factor premiums (i.e. multi-factor alphas and betas) for significantly better asset return prediction as well as algorithmic fintech network platform automation.

What differentiates our key proprietary algorithmic alpha model from most other artificial intelligence applications in quantitative finance and asset management? The vast majority of artificial intelligence methods fixate on improving predictive accuracy without sound economic rigor, intuition, and motivation. Each artificial intelligence application arises as a black box in this broad context. Each black box conveys little fundamental information about the cross-section of average asset returns. It is thus difficult, or even impossible, to establish causal linkages between factor premiums and asset prices. In this negative light, most artificial intelligence applications cannot explain why fundamental factors such as size, value, and momentum etc covary with average asset returns. Neither can these artificial intelligence applications explain why and how these covariances reflect macroeconomic news, surprises, and gyrations that manifest in the form of key dynamic conditional factor premiums across key fundamental characteristics.

We design and develop our proprietary algorithmic alpha model to fill this void both in theory and in practice. Our model not only explains why and how several fundamental factors causally explain the generic cross-section of asset returns, but it also connects dynamic conditional alphas to macroeconomic innovations, news, and surprises in key quantitative time-series tests. Specifically, our vector tests confirm mutual causation between dynamic conditional factor premiums and macroeconomic innovations, so this causation serves as a major qualifying condition for sound and robust fundamental factor selection. To the extent that macroeconomic innovations manifest in the form of dynamic conditional alphas, this causation reveals the marginal investor's fundamental news and economic expectations about the cross-section of average returns. This economic insight is our incremental step toward drawing a major distinction between rational-risk and behavioral-mispricing models.

We extend and enhance the conventional Fama-French factor model to embed fundamental factors in our proprietary algorithmic alpha system for active asset management. Such fundamental factors include size, value, momentum, asset growth, operating profitability, and market risk exposure. Each of these factors unveils a rich fraction of variation in asset returns that most purely statistical or artificial factors fail to explain both in theory and in practice. From a fundamental perspective, our proprietary algorithmic alpha model effectively gleans signals or dynamic conditional factor premiums from small profitable cash cows that go through temporary market undervaluation with conservative investment outlays in capital equipment and balance sheet expansion. In reality, we can apply this model to extract rich and valuable dynamic conditional alphas from most asset portfolios (individual U.S. stocks and both U.S. and international asset portfolios of stocks, bonds, currencies, and commodities):

Our proprietary algorithmic alpha model first extracts dynamic conditional factor premiums from the above conventional Fama-French factors. A key advantage of this model is that our chosen recursive multivariate filter allows all conditional factor premiums to dynamically adjust over time. Over each time increment, our model updates and improves predictive signals about the generic cross-section of average returns. Another major advantage of this model pertains to the fact that we can apply the same quantitative algorithm to different asset portfolios. The asset portfolios can be U.S. individual stocks as well as U.S. and non-U.S. international portfolios of stocks, bonds, currencies, and commodities. Our U.S. utility patent specification provides quantitative details on how well this dynamic conditional alpha model outperforms the static Fama-French factor models.

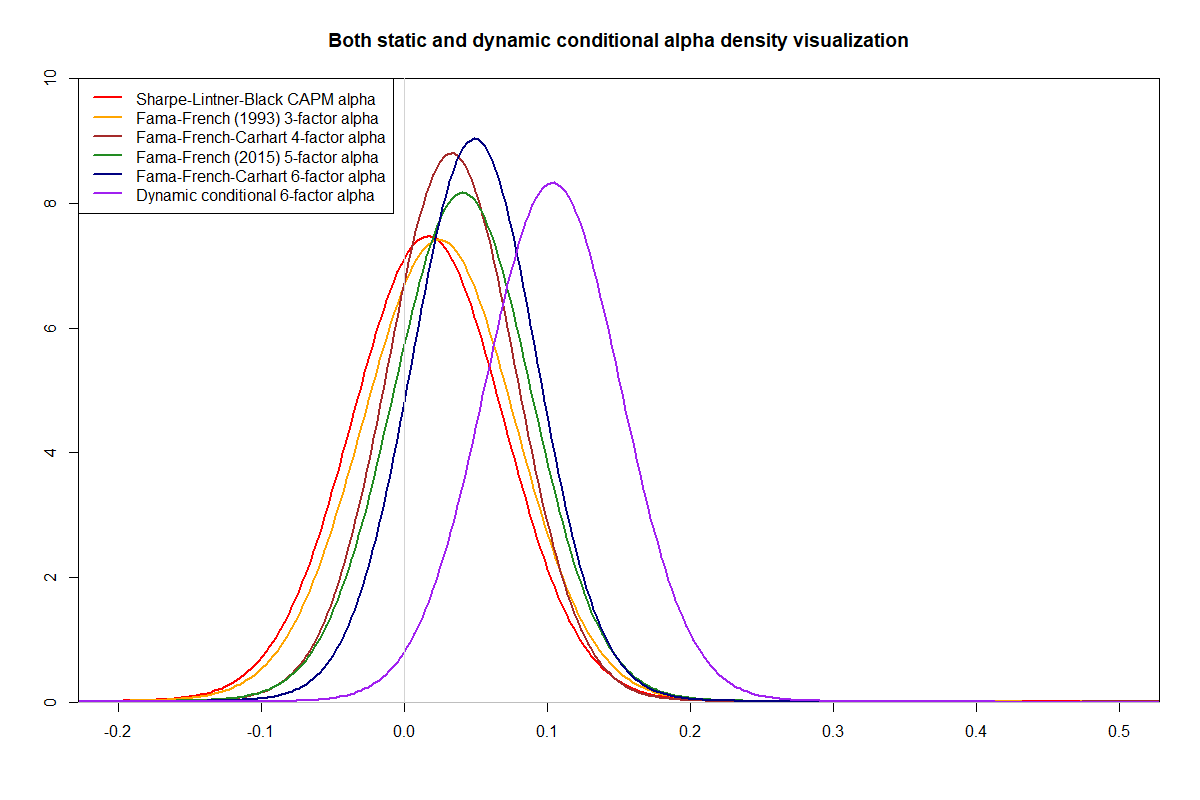

We can visualize both static and dynamic conditional alpha density distributions in the chart below. Each distribution represents the average returns on the top 6,000 U.S. stock quantiles when we rank these stocks in terms of their dynamic conditional alphas or static alphas from Fama-French multi-factor regressions. This visualization suggests that our model outperforms most prior art because dynamic conditional alphas serve as better investment signals about the cross-section of average returns. Our proprietary algorithmic alpha model attains 90% positive return likelihood, which is impressive in direct comparison to 61%-73% positive return likelihood for the prior static Fama-French factor models.

In the current invention, we design and configure the dynamic conditional asset-pricing system with a recursive multivariate filter to extract dynamic conditional factor premiums. These factor premiums turn out to be volatile alphas and betas that exhibit mutual causation with macroeconometric and cyclical innovations. Our primary patent innovation pertains to the consistent estimation of dynamic conditional factor premiums after we control for multiple explanatory factors (i.e. size, value, momentum, asset growth, profitability, and market risk exposure) through the new and unique use and implementation of a recursive multivariate filter. At most reasonable 90%, 95%, and 99% confidence levels, the dynamic conditional alphas exhibit a significantly positive relation with both Sharpe ratios and market-value-weighted average asset returns. These dynamic conditional alphas effectively explain at least 70% of the common variation in Sharpe ratios of average asset returns to standard deviations. In effect, back-of-the-envelope calculations show that our proprietary alpha model ranks U.S. individual stocks in a unique order where the stocks with the highest dynamic conditional alphas boost average annual Sharpe ratios from the U.S. stock market benchmark of 0.33 to 0.35 to a reasonable range of 0.65 to 0.85. In fact, this impressive output applies to the top decile of about 6,000 U.S. individual stocks.

Not only does our current invention recommend the dynamic conditional alpha system as a superior instrument for asset selection and portfolio optimization, but our current invention also proposes this system as a better fundamental tool for long-term asset return prediction.

Our fintech network platform automation allows users to interact with abundant proprietary financial intelligence such as dynamic conditional alpha rank order, financial ratio summary, quadripartite visualization of financial price and return data both over time and in the cross-section, financial statement analysis, and financial news search. The current invention automates the algorithmic fintech network platform via fast cloud-computing facilities for responsive web design.

With a highly modular and interactive social network, the fintech platform helps optimize active-click mutual engagement (ACME) among active users through both the centrifugal and centripetal user interactions and the time-specific rank order of each active end user's asset portfolio value appreciation ceteris paribus. ACME rises exponentially when the highly modular algorithmic fintech network platform boosts these healthy user interactions, raises the alpha ranks of some superusers, and causes significant effective changes in user-specific structural characteristics such as demographic attributes, interests, behaviors, and some other platform usage patterns. Our algorithmic fintech network platform serves as an interactive social network for all premium members to exchange relevant analytic intelligence and information. As a result, this transmission mechanism can help promote better financial literacy, inclusion, and freedom of the global general public. In this fashion, our AYA fintech network platform serves as every investor's social toolkit for profitable investment management. So we empower investors through technology, education, and social integration.

AYA fintech network platform embeds our fresh and unique dynamic conditional asset pricing system for superior risky asset return prediction, an internal cloud module for financial intelligence output, and another internal cloud module with myriad social network functions. By using this fintech network platform, all users can interact with one another by sharing rich and relevant analytical intelligence and information in order to inform better and wiser asset investment decisions. This informative transmission encapsulates each user's status updates, posts, like, unlikes, views, comments, shares, favorites, tags, invites, messages, and other web traffic statistics. Through fast and safe cloud-computing facilities for responsive web design and encryption, our current invention can automate the dynamic conditional alpha system and algorithmic social network engagement.

All our premium members can share their asset-specific views and posts within our AYA fintech network platform. Also, these members can share their asset-specific views and posts to external social networks. Examples include at least Facebook, Twitter, LinkedIn, Google+, WhatsApp, WeChat, Pinterest, Tumblr, Reddit, Flipboard, personal email, and so forth. All our premium members trade U.S. stocks with their virtual portfolio points or talents via an equivalent virtual intermediary or clearinghouse functionality. Each premium member receives an initial endowment of $1 million talents upon registration, and he or she can trade sequentially U.S. individual stocks with real-time price quotes on a daily basis.

AYA fintech network platform executes a regular maintenance method. The key elements of this regular maintenance method are curation, marquee, piggyback, and seed. The curation element refers to the essential and primary need for our platform orchestrators to filter out any adverse and undesirable social network results, patterns, outcomes, and even conflicts of interest from abusive usage to inappropriate content circulation.

The marquee element refers to backend risky asset trade history that the best 100 alpha users sequentially adapt to gain the highest up-to-date virtual talents or net overall returns per annum (NORPA). Other members who surf and trade on our fintech network platform can gradually learn from the backend history of profitable asset investment positions.

The piggyback element refers to the primary need for our platform orchestrators to allow users who currently surf on some external social networks to gravitate toward our AYA fintech network platform. At a minimum, we permit all premium members to log into our AYA fintech network platform from their Facebook and Twitter accounts. All our premium members can share their asset-specific views and posts to key external social networks. Examples include Facebook, Twitter, LinkedIn, Google+, WeChat, WhatsApp, Instagram, Pinterest, Tumblr, Reddit, Flipboard, personal email, and so forth.

The seed element pertains to the highly modular and interactive process where the best 100 alpha users engage in the progressive production and diffusion of valuable units of both financial intelligence and information through their social network interactions and activities. In the future, we plan to use several different structural methods of global newsfeed customization. Each newsfeed module caters to different member interests, behaviors, and preferences. For instance, a user-experience module helps all active members learn from the sequentially profitable asset trade histories of the best 100 alpha users who make the most productive use of virtual portfolio points or talents. An investment-style module provides key channels that segment premium members into risky asset portfolio tilts such as size, value, momentum, and so forth. A social-community module embeds multiple groups that represent unique clusters on the primary basis of demographic attributes, interests, behaviors, and other platform usage patterns.

In the meantime, we direct the next macrofinancial research endeavors toward explainable artificial intelligence. In this new direction, we integrate artificial intelligence applications such as random forests, gradient boosts, elastic nets, and principal components with our proprietary econometric omega model. This semi-parametric algorithm applies to a wide array of risky assets such as stocks, bonds, currencies, commodities, indices, and funds etc, and so helps decipher profitable asset investment signals in a fresh and unique way. We hope these macrofinancial research endeavors come to fruition in time for practical use and implementation on our AYA fintech network platform.

AYA Analytica is our online newsletter about key financial news, market insights, economic issues, and stock investment strategies on our Andy Yeh Alpha (AYA) fintech network platform. With both American focus and international reach, our primary and ultimate corporate mission aims to help enhance financial literacy, inclusion, and freedom of the open and diverse global general public. We apply our unique dynamic conditional alpha investment model as the first aid for every investor with profitable asset investment signals and portfolio strategies. In fact, our AYA freemium fintech network platform curates, orchestrates, and provides proprietary software technology and algorithmic cloud service to most members who can interact with one another on our AYA fintech network platform. Multiple blogs, posts, ebooks, analytical reports, stock alpha signals, and asset omega estimates offer proprietary solutions and substantive benefits to empower each financial market investor through technology, education, and social integration. Please feel free to sign up or login to enjoy our new and unique cloud software services on AYA fintech network platform now!!

We create each free finbuzz (or free financial buzz) as a blog post on the latest financial news and asset investment ideas. Our finbuzz collection demonstrates our unique American focus with global reach. Each free finbuzz provides deep insights into numerous topical issues in global finance, stock market investment, portfolio optimization, and dynamic asset management. We strive to help enrich the economic lives of most investors who would otherwise engage in financial data analysis with inordinate time commitment.

Please feel free to forward our finbuzz to family and friends, peers, colleagues, classmates, and others who might be keen and abuzz to learn more about asset investment strategies and modern policy reforms with macroeconomic insights.

Andy Yeh Alpha (AYA) fintech network platform serves as each investor's social toolkit for profitable investment management.

AYA fintech network platform helps promote better financial literacy, inclusion, and freedom of the global general public.

We empower investors through technology, education, and social integration.

Andy Yeh

AYA fintech network platform founder

Brass Ring International Density Enterprise (BRIDE)

Email andy.yeh.alpha@ayafintech.network service@ayafintech.network

2025-10-10 12:31:00 Friday ET

Stock Synopsis: With a new Python program, we use, adapt, apply, and leverage each of the mainstream Gemini Gen AI models to conduct this comprehensive fund

2020-09-15 08:38:00 Tuesday ET

Macro eigenvalue volatility helps predict some recent episodes of high economic policy uncertainty, recession risk, or rare events such as the recent rampan

2017-09-19 05:34:00 Tuesday ET

Facebook, Twitter, and Google executives head before the Senate Judiciary Committee to explain the scope of Russian interference in the U.S. presidential el

2021-08-01 07:26:00 Sunday ET

The Biden administration launches economic reforms in fiscal and monetary stimulus, global trade, finance, and technology. President Joe Biden proposes s

2018-09-17 12:40:00 Monday ET

Nobel Laureate Robert Shiller's long-term stock market indicator points to a recent peak. His cyclically-adjusted P/E ratio (or CAPE) accounts for long-

2027-10-31 00:00:00 Sunday ET

In the technological race between the U.S. and China, America leads in some strategic sectors from AI large language models (LLM), graphics processing units