2023-02-28 11:30:00 Tue ET

stock market federal reserve monetary policy treasury fiscal policy deficit debt bankruptcy currency dollar renminbi payment technology paypal alibaba tencent facebook covid-19 employment inflation fintech global macro outlook

As of 2022-2023, global inflation has gradually declined from the peak of 9.8% due to Fed-led interest rate hikes. Central banks view high inflation as a post-pandemic short-term aberration. As the Bank of International Settlements (BIS) shows, now 33 of 38 central banks have raised interest rates since the worldwide interest rate normalization in early-2022. Even as monetary policy starts to switch from stimulus to restraint, governments have provided more fiscal support. In recent years, these governments spend about 10% of total GDP to support most economic affairs with another 6%-worth of bank loans.

In the lofty pursuit of better inflation control, a great policy reversal is under way in OECD countries. Many central banks and governments lean toward tight monetary restraint and fiscal stimulus. The probable result is a tug-of-war between hawkish central banks and spendthrift governments. This worldwide fiscal-monetary policy coordination helps achieve the dual mandate of both price stability and maximum employment. In response to the recent stock market turmoil, this policy mix helps ensure better long-term economic growth and asset market stability.

In America, Congress has passed the new Inflation Reduction Act under the Biden administration. Meanwhile, the disinflationary effect seems marginal. The Biden cancellation of student debt can cost twice as much as the Inflation Reduction Act saves in due course. The U.S. budget deficit is likely to average almost 5% of total GDP over the next decade. The resultant annual fiscal deficits are enough to push the public-debt-to-GDP ratio to 110% by 2035. Fiscal prudence is as important as inflation control in the long run.

Around the world, many governments tend to spend freely to help households with significantly higher energy prices. This economic phenomenon is especially severe in Europe, and many European residents now need to adapt to life with much less Russian natural gas due to the Russia-Ukraine war. Germany has nationalized its biggest gas importer Uniper and then continues to spend $200 billion (or more than 5% of total GDP) on an economic defense shield with natural gas subsidies. Also, France seeks to cap energy prices with its national energy giant EDF. Britain can borrow as much as 7% of total GDP to cap energy prices in a similar vein. Although windfall tax credits can help pay for at least some of European energy expenditures, fiscal deficits are likely to rise over time. This fiscal problem pervades several Asian countries such as Japan, Malaysia, Singapore, South Korea, and Taiwan.

The pressure on governments to spend may not abate much. Ageing populations push up health care and pension outlays. After Russia’s war on Ukraine, key NATO members reiterate previously unmet promises to meet their target of spending 2% of total GDP on defense. In isolation, many of these pressures may be manageable. In combination, these social pressures require greater fiscal budgets.

In theory, big governments plus interest rate hikes are a recipe for persistently high inflation and bond market rout. It would not be wise for many governments to forgo necessary social outlays on preventing climate change, securing peace in Europe, and sustaining pension and health care reforms in the post-pandemic era. As most big governments expand their fiscal budgets, central banks may find it increasingly difficult to hit the 2% to 3% inflation targets. Governments are unlikely to stand by idly as central banks inflict pain on their domestic economies for the sake of better price stability (i.e. better inflation control). These government may instead unleash fiscal stimulus before the disinflationary task is complete.

Long-term pressures on pension and health care budgets continue to mount. The share of world population over 50 years old has grown from 15% to 25% since the 1950s, and this share is likely to exceed 40% by the end of this century. By 2035, the G20 annual pension and health care expenditures may increase by more than 5% of total GDP. It can prove to be hard for governments to control these pension and health care expenditures. All relevant reforms may mean taking on gray power at the ballot box. Many countries have chosen to raise the retirement age from 65 to 70 or even 75 as a result. This pervasive reform may not be enough to stop the length of time that most workers live in retirement worldwide.

Much of the West tends to walk the path already well-trodden by Japan (where the ageing population began in the 1990s). The Japanese pension scheme relates to pre-retirement income benchmarks and is comparable to most pension schemes in key western countries such as America, Britain, Canada, and Europe. Since the turn of the new century, the dependency ratio of people between 20 and 64 years old for every person over 64 years old has risen from 2.5 to 3.5 in Japan. America, Britain, Canada, and Europe may follow this well-trodden path in the next decades. Over the same 22-year period, the pension and health care budgets have helped propel Japan’s national debt to a vertiginous 265% of total GDP. OECD countries face the same fiscal fate in due time. In a similar vein, many other Asian countries (from Malaysia and Singapore to South Korea and Taiwan) may need to reconsider their pension and health care reforms in response to ageing populations in the next few decades.

Everywhere public debt continues to offer a tentative short-term fix. Although most ageing populations often turn out to be a drag on government budgets, these older populations also limit how high interest rates are likely to rise in the medium term. As workers approach retirement, they save and then invest in stocks, bonds, and currencies etc. Today these free and open capital investments compete for a small set of profitable business opportunities worldwide. The low and stable natural rate of interest equilibrates these global capital investments. As a consequence, many central banks strive to keep relatively low interest rates as big governments expand fiscal budgets with higher public debt burdens. This global trend seems to reverse due to the recent Fed-led interest rate normalization since early-2022.

Recent empirical studies show that ageing populations have contributed to 50% to 75% of the 2-percentage-point fall in the natural rate of interest since the 1980s. Central banks can raise real interest rates temporarily to contain inflation. However, real interest rates can remain persistently high only if the global capital investment boom balances structural shifts in demography. This mega trend may indeed tend to persist as ageing populations continue to enjoy longer longevity. In an influential book, The Great Demographic Reversal, the former central bank advisor Charles Goodhart argues that the core factor for interest rates is the global ratio of workers to pensioners. As this ratio falls in the new century, global capital investment dries up and then contributes to increases in both inflation and subsequent interest rates. With respect to higher inflation, Goodhart is the founder of the Goodhart Law in the economic science: When a measure [such as core inflation] becomes a target, this target ceases to be a good measure.

The ageing paradox pushes up government expenditures and then makes possible cost-effective fiscal finance of these expenditures (especially in pension and health care budgets). Without governments readily running up public debt burdens, the downward pressure on interest rates might have been greater in recent decades. In fact, OECD public debt has tripled between 1970 and 2023 from about 25% of total GDP to about 75% of total GDP. This public debt burden has thus left OECD interest rates 2 percentage points above where they would otherwise have been. Had the global natural rate of interest declined due to private sector behaviors and fluctuations etc, the rate might have fallen by fully 7 percentage points into negative territory. The net result would weaken the monetary policy lever for central banks as policy rates should follow the natural rate downwards to avoid deep recessions. When central banks hit the zero lower bound for interest rates (or negative shadow rates), these central banks would need to rely on large-scale asset purchases (or QE) to boost widespread economic recovery. These monetary policy principles are good lessons learnt from the Global Financial Crisis of 2008-2009.

Over time, some governments may spend forcefully enough to reduce the adverse impact of ageing populations worldwide. Nobel Laureate and former Fed chairman Ben Bernanke suggests that the recent global capital investment glut holds down long-term interest rates in America. This glut reflects the gradual accumulation of dollar reserves by key governments of Asian countries such as China, South Korea, and Taiwan. These Asian countries and OPEC oil exporters (such as Saudi Arabia) collectively seem to finance steady increases in the U.S. current account deficit in recent years.

Today, dollar reserve accumulation has slowed, and the global investment glut has become less visible in current accounts. Global capital investment imbalances are likely to return over time. This mega trend occurs when capital flows from countries with fast-ageing populations to countries with slow-ageing populations. As the U.S. transition is mild relative to the non-U.S. counterparts, America can absorb foreign capital, particularly from China, India, Japan, France, and Germany. Demographic dividends can transform into large U.S. current account deficits in due course.

How much would many OECD governments need to borrow to sop up the global investment glut? A heuristic rule of thumb is that a one-percentage-point increase in the ratio of public-debt-to-GDP for all OECD countries boosts the natural rate of interest by 3 to 5 basis points (i.e. 3 to 5 hundredths of a percentage point). During the corona virus crisis, the recent rise in public-debt-to-GDP by 40% would have increased the natural rate of interest by 1.2 to 2 percentage points.

In the meantime, the relatively low natural rate of interest would continue to allow many OECD countries to maintain high public debt mountains. Many governments should be careful how they use fiscal deficits that the global investment glut creates (especially when world crises such as the Russia-Ukraine war and pandemic crisis can strike at any time). In light of the recent world path to net zero carbon emissions, decarbonization can further weigh on fiscal budgets in the next few decades.

More than 90% of the world economy now commits to the net-zero targets for the green energy transition. Around the world, roads need ubiquitous charging-points for electric vehicles, and these energy-efficient vehicles can help replace internal combustion engines. Above all, power grids are often clean and green to cope with higher demand when everything runs on electricity. Advocates of climate change investments have already presented this power energy efficiency as an advantage. Big infrastructure investments would be part of the green new deal for better long-term returns in excess of interest costs. The Biden administration suggests that a green investment push can help boost both U.S. demand and employment for the economic recovery from the Covid-19 pandemic crisis. The Inflation Reduction Act provides the largest slug of climate change expenditures in America. In effect, the Inflation Reduction Act can help reduce the U.S. fiscal deficit by raising corporate income taxes with better tax enforcement.

Under the Biden administration, the Inflation Reduction Act would reduce U.S. net carbon emissions by more than 30% from 2005 to 2030. This net carbon reduction accords with the Biden long-term target of a 50% cut. Climate change investments are quite affordable for 3 main reasons. First, the world continually replaces boilers, cars, and even power plants regardless of any green energy transition. Incremental fiscal expenditures are often much lower than the gross costs of alternative energy sources. A recent McKinsey survey shows that an annual average of 9% of world GDP must be spent on green assets to achieve net-zero carbon emissions by 2050. Over the next decade, essential climate change investments represent at least 3% to 5% of cumulative world output.

Second, the private sector can pick up much of the tab (regardless of public sector subsidies). Households buy their own boilers and cars, and private companies are responsible for more than 90% of all energy investments in power grids and plants. The IMF suggests that the basic need for public-sector climate change investments further hovers in the range of 2% to 5% of cumulative world output between 2023 and 2035. For the green energy transition, fiscal expenditures depend on whether several other relevant policies are in place to encourage the private sector to invest in green tech advances such as lithium-ion batteries, electric cars, and hydropower plants etc. In free open capitalist societies, households and businesses put money to work where the returns are greatest (in accordance with the Coase Theorem). These private-sector market players pony up cash for net-zero carbon emissions only if there are sufficient incentives for this compliance. Carbon prices help tilt the scales in favor of green climate change investments. A common market failure to price carbon can be doubly costly. This market failure often forces the public sector to shoulder more of the burden of climate change investments. As a consequence, this pervasive market failure may inadvertently deprive the government of taxable income from households and businesses. In America, for instance, personal taxes have been kept constant in cash terms since 1993 and federal carbon prices seem unlikely to pass Congress. For the next decade between 2023 and 2033, the Biden administration has approved tax credits for electric vehicles as part of the landmark Inflation Reduction Act. The stick of carbon prices would make the carrot of public-sector subsidies less necessary. However, most current carbon prices remain too low. Every dollar on the carbon price makes climate change investments in clean and green energy sources more attractive for the private sector.

Third, the green transition pays off not only in terms of lower extreme weather and rare disaster risks, but also through greater efficiency gains in due course. Relative to internal combustion engines, electric vehicles rely less on electromagnetic fluids. Also, electric cars require less maintenance. With greater energy efficiency, these electric cars cause lower operational costs. Should battery technology continue to advance with better lithium chargers, electric cars are likely to eventually become more cost-effective than petrol cars. The long-term benefits are likely to be enough to outweigh the short-term costs of weaning the world economy off fossil fuels.

The rich world plus China now account for about 67% of annual carbon emissions. If the world seeks to achieve net-zero carbon emissions without hamstringing the economic prospects of billions of people, the rich world must help many developing countries decarbonize as these economies grow in due time. As the Paris climate agreement suggests, the rich world should provide $100 billion each year of both public and private finance to help most developing countries launch climate change investments. These green investments focus on minimizing the economic costs of both extreme weather and rare disaster risks. Meeting this climate target is not just a diplomatic challenge, but also a technical one. Indeed, this challenge reflects the difficulty of promoting climate change investments in developing countries with less protection of property rights.

In normal times, the argument for debt finance of most climate change investments would be strong. It can be more efficient for governments to spread costs over time. This common approach is often more cost-effective than paying for a green splurge with sharply higher taxes. In recent times, high inflation means that it is no longer a good time for governments to raise fiscal deficits for climate change investments. The cash available for green investments may often depend on whether politicians decide to join central banks in their present fight against inflation.

Many countries have become less equal since the 1980s. This economic inequality helps explain why the natural rate of interest has fallen worldwide. Wealthy people save more as a fraction of their income, and most of this income arises from capital investments in stocks, bonds, mutual funds, currencies, and other risky assets etc. As these wealthy capitalists earn a bigger slice of the economic pie, global capital investments increase in due course. The American economy now suffers a global investment glut of the rich. About 67% of this global investment glut helps finance the public debt of the U.S. government.

Rising inequality can cause OECD economies to fall into the debt trap. The global investment glut of the rich pushes down interest rates and then encourages other sectors to borrow for the current capital investment boom. Over time, the additional returns on capital investments allow the rich to earn more capital income and rent. As a consequence, the cycle starts again, and real interest rates fall further. Short-term macro policies such as deficit-driven fiscal stimulus programs and low interest rates result in even more public debt. When this public debt becomes due in time, the economy faces lower interest rates and worse recessions in the future.

In recent times, many central banks continue to raise interest rates to fight inflation. OECD countries have become more sensitive to higher interest rates and severe recessions. Over time, the debt trap keeps low and stable real interest rates. Macro finance models from habit formation and long-run risk to rare disaster risk etc seek to explain the 6% equity risk premium puzzle, the 1% risk-free rate puzzle, and the 29% asset market volatility puzzle. As the representative agent updates his or her expectations of both consumption growth and recession risks, the high equity risk premium tends to persist in the new era of steady interest rate hikes.

Many OECD countries experience a significance increase in the household-debt-to-GDP ratio from about 80% a decade ago to more than 110% in 2022-2023. Half of household debt links to short-term interest rates. The higher level of household debt would be enough to lop an additional 10% off government expenditures if real interest rates return to the reasonable range of 4.5% to 5.5%.

How can OECD economies escape this debt trap? Only a significant reduction in wealth and income inequality can help governments avoid the debt trap (through fiscal transfers, structural reforms, or redistributive taxes). Indeed, inflation serves as another similar market force. Inflation redistributes wealth and income from key creditors to debtors so long as this redistribution leads to stronger wage growth for debtors. From time to time, economists view inflation as a veil or a nominal but not real economic phenomenon. If central banks cannot tame price increases in time, inflation continues to transfer real wealth and income from creditors to debtors. In due course, this redistribution might shatter the fundamental prospects of the world economy.

Nobel Laureate Milton Friedman proposes the economic cycle of both output and inflation through boom-bust fluctuations. Loose and abundant money first creates a boom and then inflation. A new outcry against price hikes leads to higher interest rates. The economy departs from full employment and then enters a recession. In response, the government provides fiscal stimulus. As inflation declines in due time, another boom kicks off. The Friedman inflationary cycle starts again.

The world economy is now in the early stages of the Friedman inflationary cycle. Inflation has often played havoc with central bank credibility and then has crushed consumer confidence. In Europe, high gas prices can cause economic turmoil this winter. European consumers are now more miserable during the Russia-Ukraine war than they used to be during past financial crises. In East Asia, dearer oil and currency depreciation have forced central banks to raise interest rates in tandem with gradual Fed-led rate hikes. Around the world, monetary policy-makers focus on the single enemy of higher inflation in the form of pervasive price increases. As the hawkish monetary policy stance takes its toll, the disinflationary ripple effects flow through many OECD countries. These macro developments can complete the Friedman cycle of both output and inflation through boom-bust fluctuations.

Headline inflation has declined from its recent peak in America. Even European oil and natural gas prices have fallen in recent times. Key economists compare annual wage growth to annual productivity growth since 2001. The gap between these 2 composite measures seems largest in the Anglosphere: this gap ranges from 3.8% to 4.6% in America, Britain, Canada, and New Zealand. In the Euro zone, the gap hovers around 2.4%. By comparison, the gap is a little over 1% in most East Asian countries such as Japan, Malaysia, Singapore, South Korea, and Taiwan.

As shown in a new survey of 10 American disinflationary episodes since the 1950s, a median decline in U.S. core inflation of 2 percentage points tends to arise from an increase in unemployment of 3.6 percentage points over a 30-month period. In the typical disinflationary scenario, 6 million Americans lose their jobs. Empirical studies further show that unemployment might need to rise by 5 percentage points each year to bring inflation down a single percentage point. The short-term trade-off between inflation and unemployment seems weaker in Britain, Canada, Europe, Australia, and New Zealand. For this technical reason, many economists prefer to focus on the key New Keynesian Phillips Curve, i.e. the mysterious and inexorable trade-off between wage inflation and unemployment. In this fresh light, the Federal Reserve System and European Central Bank would require about 50-to-75-basis-point interest rate hikes to tame inflation. This pervasive inflationary scenario is less acute elsewhere in the world.

Macro economists often consider 2 additional macro conditions for inflation control. The first macro condition pertains to how much inflation expectations drift upward as inflation continues to persist above the Fed-led 2% average target. The second macro condition relates to whether the domestic labor market can cool off in time not by shedding jobs but by shedding job vacancies. U.S. job vacancies have been extraordinarily high during the recent recovery from Covid-19. If the current interest rate hikes help bring down inflation to the reasonable range of 1.6% to 3.2% by the end of 2024, U.S. unemployment is likely to rise to 7.5% for the next 2 years. These estimates accord with the Fed-led dual macro mandate of both price stability and maximum employment.

In fact, there is no need for the Federal Reserve System to generate a recession on purpose. The main macro mandate is to stop higher import prices from setting off a wage-price spiral. With oil price declines, the global economic slowdown has made inflation less likely to rise further. Many central banks now need to think hard about the New Keynesian mysterious and inexorable trade-off between inflation and unemployment. Some real business cycle (RBC) proponents suggest that the Phillips curve has become the Phillips cloud in recent times. In this alternative view, there is no real trade-off between inflation and unemployment in the long-run, and the total welfare cost of inflation becomes minimal in the medium term.

The Sargent-Wallace unpleasant monetarist arithmetic analysis demonstrates that the central bank cannot contain money supply growth (or high inflation) if the fiscal authority engages in endless government bond issuance to fund public investment projects for better economic growth and employment. In this case, the central bank loses its monetary policy independence due to a lack of fiscal prudence. As a result, the central bank would eventually tolerate higher inflation sooner or later as money supply growth (or so inflation) accelerates due to the gradual accumulation of fiscal deficits over time. In effect, national debt caps constrain the positive fruits of macro policy coordination between the central bank and the fiscal authority.

The world economy now needs better fiscal-monetary policy coordination. Central banks would use monetary policy decisions and interest rate adjustments to keep inflation on target (typically at 2% to 3%). Governments would keep debt caps and fiscal deficits under control to focus on supply-side economic reforms. Long before the corona virus crisis, many economists have been arguing in favor of a modest increase in the inflation target from 2% to 3% (or 4%) to boost interest rates above the zero lower bound. This incremental reform builds up monetary policy firepower in due course.

Today, it would be simple for each central bank to make a change of inflation target. Monetary policy-makers should reduce inflation to at least 4% with a regime switch from the hawkish to dovish macro policy stance. Although monetary policy would be more dovish in the short run, interest rates would eventually settle higher than these rates would have been under the 2% average inflation target. In time, central banks should transform the dual mandate into a trilemma: monetary policy-makers make interest rate adjustments in response to output, inflation, and asset market fluctuations over time.

Today inflation is a monetary phenomenon worldwide. With the likely expectations of both output and employment, high inflation may inadvertently become a serious self-fulfilling macro problem. For now the Federal Reserve System’s only option is to continue to make inflation its top macro policy priority. The risk of an unknown potential breakage in asset markets is not a near-term reason for the central bank to preemptively pull back on fighting inflation when the problem of pervasive price hikes is this acute. Instead of asset market stability concerns, the more compelling argument for hawkish monetary policy is that it takes time for interest rate hikes to help contain inflation in the next 2 to 3 years.

Financial stability concerns should weigh more on monetary policy decisions when the Federal Reserve System is reasonably close to achieving the dual mandate of both price stability and maximum sustainable employment. However, economists should not discount financial stability risks today. Large banks and other financial institutions should hold substantially higher core equity capital in order to absorb extreme losses that might arise in rare times of severe financial stress. In a recent inflationary world, the Federal Reserve System cannot accomplish much because any Fed put interest rate adjustments may inevitably trip over the dual mandate. A relatively optimistic macro scenario over the next 2 years is that U.S. interest rates reach the reasonable range of 5% to 5.5% with 3.5%-4% core inflation and 5.5% unemployment. Through a mild recession, America, Britain, Canada, and Europe etc can traverse the steep part of the Phillips curve. At that point, it would be highly difficult for OECD central banks to further reduce inflation without job losses. The sacrifice ratio becomes too high to be consistent with the dual mandate.

Central banks should transform the dual mandate into a trilemma: monetary policy-makers make interest rate adjustments in response to output, inflation, and asset market fluctuations over time. In addition to the dual mandate, recent interest rates adjustments should help restrain credit supply hikes and asset price increases. In time, central banks can combine monetary policy decisions and macro-prudential instruments (such as loan-to-value debt-income ratios) to smooth out the financial accelerator cycle. Sometimes central banks may launch interest rate hikes to lean against to wind for asset market stabilization. Around the world, central banks may likely conclude the current cycle of interest rate hikes before asset market stability concerns arise in due course. These financial stability concerns often force central banks to recalibrate the hawkish-to-dovish monetary policy stance worldwide.

As of 2022-2023, global inflation has gradually declined from the peak of 9.8% due to Fed-led interest rate hikes. Central banks view high inflation as a post-pandemic short-term aberration. As the Bank of International Settlements (BIS) shows, now 33 of 38 central banks have raised interest rates since the worldwide interest rate normalization in early-2022. Even as monetary policy starts to switch from stimulus to restraint, governments have provided more fiscal support. In recent years, these governments spend about 10% of total GDP to support most economic affairs with another 6%-worth of bank loans.

In the lofty pursuit of better inflation control, a great policy reversal is under way in OECD countries. Many central banks and governments lean toward tight monetary restraint and fiscal stimulus. The probable result is a tug-of-war between hawkish central banks and spendthrift governments. This worldwide fiscal-monetary policy coordination helps achieve the dual mandate of both price stability and maximum employment. In response to the recent stock market turmoil, this policy mix helps ensure better long-term economic growth and asset market stability.

In America, Congress has passed the new Inflation Reduction Act under the Biden administration. Meanwhile, the disinflationary effect seems marginal. The Biden cancellation of student debt can cost twice as much as the Inflation Reduction Act saves in due course. The U.S. budget deficit is likely to average almost 5% of total GDP over the next decade. The resultant annual fiscal deficits are enough to push the public-debt-to-GDP ratio to 110% by 2035. Fiscal prudence is as important as inflation control in the long run.

Around the world, many governments tend to spend freely to help households with significantly higher energy prices. This economic phenomenon is especially severe in Europe, and many European residents now need to adapt to life with much less Russian natural gas due to the Russia-Ukraine war. Germany has nationalized its biggest gas importer Uniper and then continues to spend $200 billion (or more than 5% of total GDP) on an economic defense shield with natural gas subsidies. Also, France seeks to cap energy prices with its national energy giant EDF. Britain can borrow as much as 7% of total GDP to cap energy prices in a similar vein. Although windfall tax credits can help pay for at least some of European energy expenditures, fiscal deficits are likely to rise over time. This fiscal problem pervades several Asian countries such as Japan, Malaysia, Singapore, South Korea, and Taiwan.

The pressure on governments to spend may not abate much. Ageing populations push up health care and pension outlays. After Russia’s war on Ukraine, key NATO members reiterate previously unmet promises to meet their target of spending 2% of total GDP on defense. In isolation, many of these pressures may be manageable. In combination, these social pressures require greater fiscal budgets.

In theory, big governments plus interest rate hikes are a recipe for persistently high inflation and bond market rout. It would not be wise for many governments to forgo necessary social outlays on preventing climate change, securing peace in Europe, and sustaining pension and health care reforms in the post-pandemic era. As most big governments expand their fiscal budgets, central banks may find it increasingly difficult to hit the 2% to 3% inflation targets. Governments are unlikely to stand by idly as central banks inflict pain on their domestic economies for the sake of better price stability (i.e. better inflation control). These government may instead unleash fiscal stimulus before the disinflationary task is complete.

As of mid-2022, we provide our proprietary dynamic conditional alphas for the U.S. top tech titans Meta, Apple, Microsoft, Google, and Amazon (MAMGA). Our unique proprietary alpha stock signals enable both institutional investors and retail traders to better balance their key stock portfolios. This delicate balance helps gauge each alpha, or the supernormal excess stock return to the smart beta stock investment portfolio strategy. This proprietary strategy minimizes beta exposure to size, value, momentum, asset growth, cash operating profitability, and the market risk premium. Our unique proprietary algorithmic system for asset return prediction relies on U.S. trademark and patent protection and enforcement.

Our unique algorithmic system for asset return prediction includes 6 fundamental factors such as size, value, momentum, asset growth, profitability, and market risk exposure.

Our proprietary alpha stock investment model outperforms the major stock market benchmarks such as S&P 500, MSCI, Dow Jones, and Nasdaq. We implement our proprietary alpha investment model for U.S. stock signals. A comprehensive model description is available on our AYA fintech network platform. Our U.S. Patent and Trademark Office (USPTO) patent publication is available on the World Intellectual Property Office (WIPO) official website.

Our core proprietary algorithmic alpha stock investment model estimates long-term abnormal returns for U.S. individual stocks and then ranks these individual stocks in accordance with their dynamic conditional alphas. Most virtual members follow these dynamic conditional alphas or proprietary stock signals to trade U.S. stocks on our AYA fintech network platform. For the recent period from February 2017 to February 2022, our algorithmic alpha stock investment model outperforms the vast majority of global stock market benchmarks such as S&P 500, MSCI USA, MSCI Europe, MSCI World, Dow Jones, and Nasdaq etc.

This analytic essay cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, personal finance tools, and other self-help inspirations. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

We share and circulate these informative posts and essays with hyperlinks through our blogs, podcasts, emails, social media channels, and patent specifications. Our goal is to help promote better financial literacy, inclusion, and freedom of the global general public. While we make a conscious effort to optimize our global reach, this optimization retains our current focus on the American stock market.

This free ebook, AYA Analytica, shares new economic insights, investment memes, and stock portfolio strategies through both blog posts and patent specifications on our AYA fintech network platform. AYA fintech network platform is every investor's social toolkit for profitable investment management. We can help empower stock market investors through technology, education, and social integration.

We hope you enjoy the substantive content of this essay! AYA!

Andy Yeh

Chief Financial Architect (CFA) and Financial Risk Manager (FRM)

Brass Ring International Density Enterprise (BRIDE) ©

Do you find it difficult to beat the long-term average 11% stock market return?

It took us 20+ years to design a new profitable algorithmic asset investment model and its attendant proprietary software technology with fintech patent protection in 2+ years. AYA fintech network platform serves as everyone's first aid for his or her personal stock investment portfolio. Our proprietary software technology allows each investor to leverage fintech intelligence and information without exorbitant time commitment. Our dynamic conditional alpha analysis boosts the typical win rate from 70% to 90%+.

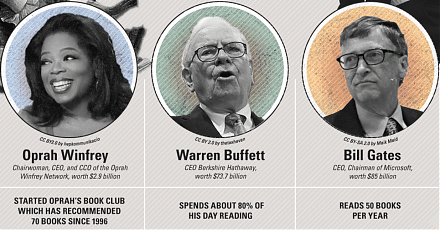

Our new alpha model empowers members to be a wiser stock market investor with profitable alpha signals! The proprietary quantitative analysis applies the collective wisdom of Warren Buffett, George Soros, Carl Icahn, Mark Cuban, Tony Robbins, and Nobel Laureates in finance such as Robert Engle, Eugene Fama, Lars Hansen, Robert Lucas, Robert Merton, Edward Prescott, Thomas Sargent, William Sharpe, Robert Shiller, and Christopher Sims.

Follow our Brass Ring Facebook to learn more about the latest financial news and fantastic stock investment ideas: http://www.facebook.com/brassring2013.

Free signup for stock signals: https://ayafintech.network

Mission on profitable signals: https://ayafintech.network/mission.php

Model technical descriptions: https://ayafintech.network/model.php

Blog on stock alpha signals: https://ayafintech.network/blog.php

Freemium base pricing plans: https://ayafintech.network/freemium.php

Signup for periodic updates: https://ayafintech.network/signup.php

Login for freemium benefits: https://ayafintech.network/login.php

We update and refresh part of memetic financial information on a sporadic basis. We aim to facilitate this information exchange only for illustrative purposes. Some information may be stale and incomplete. Therefore, we recommend each member to consult the respective external website(s) for more up-to-date information.

This analytic report cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, and other financial issues. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

The conventional disclaimers apply to this key case where each freemium member bewares, understands, and acknowledges the service terms and conditions for our courteous fintech network platform. Any omissions, errors, or other blemishes do not necessarily reflect the official views and opinions of our AYA fintech platform orchestrator. We make a conscious effort to keep most major omissions to 1% to 5% of the fintech information for about 6,000 U.S. stocks on NYSE, NASDAQ, and AMEX. These omissions tend to concentrate around some rare corporate events (e.g. IPO, delisting occurrence and recurrence, abrupt trading suspension, and M&A initiation etc). Overall, these disclaimers, terms, and conditions of our service should be viewed as baseline house rules for fintech network platform usage and development.

Under pending subsequent patent-law confirmation, the relevant legal text protects our proprietary alpha software technology for ubiquitous knowledge transfer. Each freemium member enjoys his or her interactive usage and information exchange on our AYA algorithmic fintech network platform with sound and efficient dynamic conditional asset return prediction.

Our AYA fintech network platform helps promote better financial literacy, inclusion, and freedom of the global general public with an abiding interest in core economic reforms, financial markets, and stock market investments. In this broader context, each freemium member can consult our mission statement that provides more in-depth explanatory details on our long-term aspiration.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2017-12-07 08:31:00 Thursday ET

Large multinational tech firms such as Facebook, Apple, Microsoft, Google, and Amazon can benefit much from the G.O.P. tax reform. A recent stock research r

2017-02-25 06:44:00 Saturday ET

As the White House economic director, Gary Cohn suggests that the Trump administration will tackle tax cuts after the administration *repeals and replaces*

2025-06-21 05:25:00 Saturday ET

President Trump refreshes American fiscal fears, worries, and concerns through the One Big Beautiful Bill Act. The Congressional Budget Office (CBO) estimat

2017-12-21 12:45:00 Thursday ET

Tony Robbins summarizes several personal finance and investment lessons for the typical layperson: We cannot beat the stock market very often, so it w

2019-09-30 07:33:00 Monday ET

AYA Analytica finbuzz podcast channel on YouTube September 2019 In this podcast, we discuss several topical issues as of September 2019: (1) Former

2019-02-07 07:25:00 Thursday ET

President Trump picks David Malpass to run the World Bank to curb international multilateralism. The Trump administration seems to prefer bilateral negotiat