2018-08-21 11:40:00 Tue ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

President Trump criticizes his new Fed Chair Jerome Powell for accelerating the current interest rate hike with greenback strength. This criticism overshadows the murky independence of the U.S. Federal Reserve System.

Monetary policy independence often contributes to the real effects of incremental interest rate adjustments on economic output, employment, and capital investment. This political independence is important with respect to the Lucas-Sargent-Wallace monetary invariance principle. This monetary invariance principle suggests that if only unpredictable money supply changes move real economic variates, monetary policy decisions that generate systematic or predictable variation in money supply would have no real impact on economic variates such as output, employment, and consumption. The subsequent relevant real business cycle (RBC) model variants play an important role in the key analysis of time inconsistency of optimal monetary policy conduct. Central bank independence and credibility thus become important institutional determinants of what constitutes effective monetary policy decisions.

A recent Oxford Economics research note by Alberto Alesina and Larry Summers affirms the empirical fact that most OECD countries experience high inflation (and maybe high unemployment) with subpar monetary policy independence. Several past examples of political influence over monetary policy decisions relate to the Nixon and Bush administrations.

For instance, President Nixon swapped out Former Fed Chair William McChesney Martin with his presidential pick Arthur Burns. The Nixon tapes revealed numerous conversations between Nixon and Burns where Nixon required the Fed chairman to keep low interest rates in order to maintain high employment in the 1970s. Nixon even indicated to his advisers that the administration could tolerate inflation but not high unemployment. As he tried to tilted the New Keynesian Phillips Curve (NKPC), Nixon's subsequent monetary policy stance proved to be disastrous as it ushered in a multi-year period of stagflation (i.e. high inflation, high unemployment, and low economic growth).

Later President George H.W. Bush often complained about the hawkish monetary policy decisions of his Fed chairman Alan Greenspan in the early-1990s. However, these complaints were less aggressive as Greenspan was able to assuage the dovish concern and suspicion that several senators shared back then.

At Jackson Hole, both Kansan City and Cleveland Fed CEOs Esther George and Loretta Mester point out that it is unlikely for the Trump administration to prevent subsequent interest rate hikes after mid-2018. Most monetary policy pundits and experts now predict one interest rate hike in September 2018 and another hike in December 2018. This prediction accords with the Wall Street consensus among top investment banks such as Goldman Sachs, JPMorgan Chase, Citigroup, UBS, and Bank of America.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2018-11-17 09:33:00 Saturday ET

Zillow share price plunges 20% year-to-date as its competitors Redfin and Trulia also experience an economic slowdown in the real estate market. The real es

2018-01-19 11:32:00 Friday ET

Most major economies grow with great synchronicity several years after the global financial crisis. These economies experience high stock market valuation,

2017-12-19 09:39:00 Tuesday ET

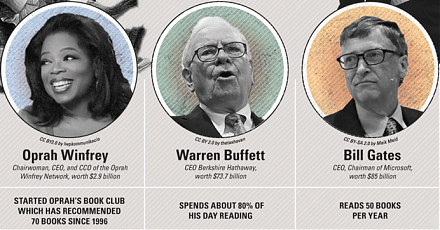

From Oprah Winfrey to Bill Gates, this infographic visualization summarizes the key habits and investment styles of highly successful entrepreneurs:

2022-08-30 10:32:00 Tuesday ET

The financial services industry needs fewer banks worldwide. As long as banks have existed in human history, their managers have realized how not all dep

2022-03-15 10:32:00 Tuesday ET

Capital structure theory and practice The genesis of modern capital structure theory traces back to the seminal work of Modigliani and Miller (1958

2019-02-03 13:39:00 Sunday ET

It can be practical for the U.S. to impose the 2% wealth tax on the rich. Democratic Senator Elizabeth Warren proposes a 2% wealth tax on the richest Americ