2019-09-23 12:25:00 Mon ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

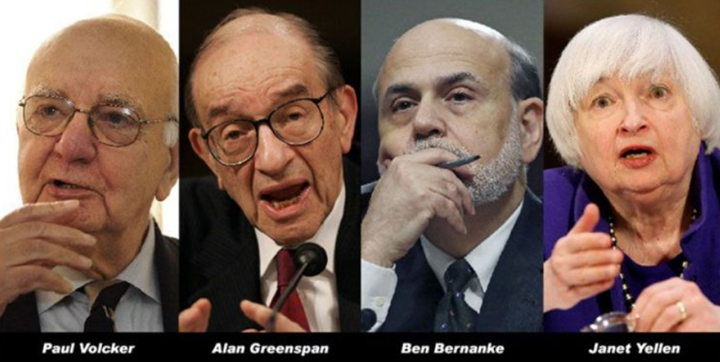

Volcker, Greenspan, Bernanke, and Yellen contribute to a Wall Street Journal op-ed on monetary policy independence. These former Federal Reserve chiefs unite together to express their core concern that Fed Chair Jerome Powell institutes the recent dovish interest rate decrease in response to a vocal president. In their joint conviction, the Federal Reserve and its chair must be able to make monetary policy decisions in the best interests of the U.S. economy. Further, these monetary policy decisions must be independent and free of short-term political pressure without the threat of either removal or demotion of Federal Reserve leaders for non-economic reasons. Volcker, Greenspan, Bernanke, and Yellen emphasize the congressional checks and balances with respect to the Federal Reserve monetary policy purview.

In recent times, Fed Chair Jerome Powell and FOMC members approve a quarter-point interest rate decrease to help sustain the current U.S. economic expansion. This monetary policy decision arises in the broader context of relentless criticisms among the Trump hawkish hardliners. The hardliners and President Trump himself view the prior U.S. interest rate hikes as headwinds that may inadvertently offset the economic benefits of Trump tax incentives and other fiscal stimulus packages for better infrastructure, investment, and technology.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2022-02-25 00:00:00 Friday ET

Empirical tests of multi-factor models for asset return prediction The capital asset pricing model (CAPM) of Sharpe (1964), Lintner (1965), and Bla

2019-01-03 10:38:00 Thursday ET

American parents often worry about money and upward mobility for their children. A recent New York Times survey suggests that nowadays American parents spen

2019-07-21 09:37:00 Sunday ET

Facebook introduces a new cryptocurrency Libra as a fresh medium of exchange for e-commerce. Libra will be available to all the 2 billion active users on Fa

2017-09-13 10:35:00 Wednesday ET

CNBC reports the Top 5 features of Apple's iPhone X. This new product release can be the rising tide that lifts all boats in Apple's upstream value

2019-03-11 10:32:00 Monday ET

Lyft seeks to go public with a dual-class stock ownership structure that allows the co-founders to retain significant influence over the rideshare tech unic

2019-07-05 09:32:00 Friday ET

Warwick macroeconomic expert Roger Farmer proposes paying for social welfare programs with no tax hikes. The U.S. government pension and Medicare liabilitie