2018-06-08 13:35:00 Fri ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

The Federal Reserve delivers a second interest rate hike to 1.75%-2% and then expects subsequent rate increases in September and December 2018 to dampen inflationary pressures. This decision reflects robust economic revival in America. With sound price stability, the U.S. economy now operates near full employment with 2.1% inflation and 3.8% unemployment (i.e. the lowest unemployment rate since 2000). The current real economic growth trajectory accords with the Federal Reserve's dual mandate of maximum employment and price stability.

The Federal Reserve pencils in subsequent interest rate hikes later in 2018 (2%-2.25% in September 2018 and then 2.25%-2.5% in December 2018). This gradual acceleration of interest rate increases helps contain inflation with steady gains in the labor market. The current interest rate hike might disappoint President Trump who would otherwise prefer dovish monetary policy accommodation (in contrast to hawkish inflation containment).

However, the Federal Reserve reiterates monetary policy independence and thus continues the current interest rate hike as the U.S. economy moves along the long-run steady-state economic growth path of healthy fundamental recalibration. On balance, it is now quite plausible for America to achieve 3%+ real GDP economic growth to better balance the U.S. fiscal budget that helps neutralize both trade and budget deficits in the medium term.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2019-01-21 10:37:00 Monday ET

Andy Yeh Alpha (AYA) AYA Analytica financial health memo (FHM) podcast channel on YouTube January 2019 In this podcast, we discuss several topical issues

2018-03-17 09:35:00 Saturday ET

Facebook faces a major data breach by Cambridge Analytica that has harvested private information from more than 50 million Facebook users. In a Facebook pos

2018-12-22 14:38:00 Saturday ET

Federal Reserve raises the interest rate to the target range of 2.25% to 2.5% as of December 2018. Fed Chair Jerome Powell highlights the dovish interest ra

2017-10-03 18:39:00 Tuesday ET

President Trump has nominated Jerome Powell to run the Federal Reserve once Fed Chair Janet Yellen's current term expires in February 2018. Trump's

2019-01-19 12:38:00 Saturday ET

U.S. government shuts down again because House Democrats refuse to spend $5 billion on the border wall that would give President Trump great victory on his

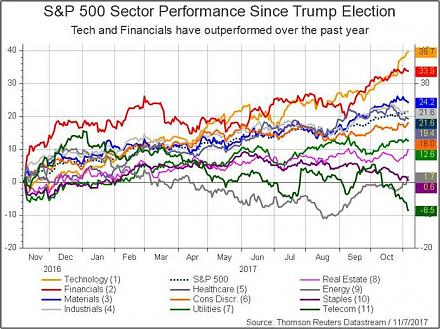

2017-10-09 09:34:00 Monday ET

The current Trump stock market rally has been impressive from November 2016 to October 2017. S&P 500 has risen by 21.1% since the 2016 presidential elec