2018-07-21 13:35:00 Saturday ET

President Trump supports a bipartisan bill or the Foreign Investment Risk Review Modernization Act (FIRRMA), which effectively broadens the jurisdiction of

2023-11-30 08:29:00 Thursday ET

In addition to the OECD bank-credit-card model and Chinese online payment platforms, the open-payments gateways of UPI in India and Pix in Brazil have adapt

2019-12-30 11:28:00 Monday ET

AYA Analytica finbuzz podcast channel on YouTube December 2019 In this podcast, we discuss several topical issues as of December 2019: (1) The Trump adm

2019-11-15 13:34:00 Friday ET

The Economist offers a special report that the new normal state of economic affairs shines fresh light on the division of labor between central banks and go

2019-08-31 14:39:00 Saturday ET

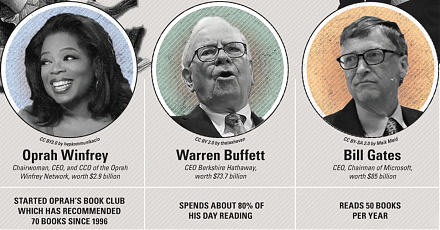

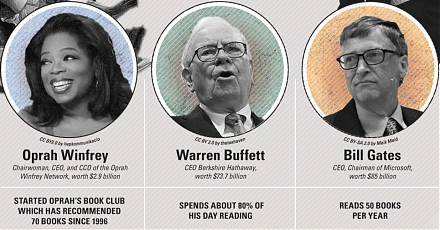

AYA Analytica finbuzz podcast channel on YouTube August 2019 In this podcast, we discuss several topical issues as of August 2019: (1) Warren B

2019-10-17 08:35:00 Thursday ET

The European Central Bank expects to further reduce negative interest rates with new quantitative government bond purchases. The ECB commits to further cutt