2023-08-14 09:25:00 Mon ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession financial crisis systemic risk asset market stabilization economic growth central bank fomc forward guidance euro capital global financial cycle bank capital regulation

Peter Isard (2005)

Globalization and the international financial system

Peter Isard provides his prescient overview of empirical work on the past operation and reforms of the international monetary and financial system. Isard draws macro policy lessons from the global economic history of both exchange rates and capital flows (especially from the financial crises of the 1990s and 2008-2009). In light of the current international monetary and financial environment, Isard delves into the ongoing debate over the joint stewardship of both the World Bank and International Monetary Fund (IMF). In a fundamental view, financial crises and economic growth failures occur with unacceptable frequency. Isard analyzes what policymakers can accomplish in order to strengthen the global macro financial system. Isard further demystifies the IMF puzzle by addressing the central criticisms of IMF activities in recent decades. Financial globalization can be a sustainable engine of economic growth. At the same time, financial globalization may inadvertently cause financial fragility in the global network of capital flows. Isard thus focuses on the core capital markets and policies, exchange rates, private investment decisions, and regulatory agencies. These inclusive institutions help shape the current account balances and capital flows. The IMF supports different flexible exchange rate regimes, monetary policy systems, capital flows, and financial crisis resolution paths.

As a former senior advisor at the IMF, Isard provides his macro economic insights into exchange rate regimes, capital flows, and macrofinancial crises. Many modern macro models can help predict exchange rate fluctuations over long time horizons. Isard attributes several financial crises of the 1990s and the Global Financial Crisis of 2008-2009 to persistent exchange rate misalignments, substantial fiscal budget and current account deficits, weak bank systems, and unsustainable national debt burdens. Sometimes financial crises turn out to be both chaotic and unpredictable black swan rare events due to self-reinforcing prophecies, beliefs, and preferences. International monetary and financial reforms can take much time and cross-country coordination and collaboration. There are many different ways for economists and politicians to skin the cat, and all roads eventually lead to Rome. However, no one can build Rome in one day.

Isard analyzes cross-border capital flows by applying modern macro models to the advantages of global capital mobility for smoothing consumption, sharing risk, and relaxing financial constraints. In this fundamental view, opening an economy to the cross-border capital flows can help enhance economic welfare only if this core step follows the installation of essential preconditions. Such preconditions include open free trade, clear macro mandate equivalence between price stability and economic growth, rigorous prudential supervision, bank intermediary capital regulation, and effective corporate governance. Further, inclusive institutions empower economic actors to apply their skills and talents to promote economic growth, full employment, general price stability, and asset market stabilization etc. Volatile short-term capital flows can interact with external distortions to heighten financial fragility. From time to time, fiscal stimulus, taxation, and bank capital regulation can contribute to more effective monetary policy steps in pursuit of better economic growth, employment, capital investment, high-skill knowledge-intensive human capital accumulation, or general price stability in the traditional sense.

Foreign direct investment (FDI) tends to offer the merit of applying organizational and technological knowledge to non-OECD countries. These non-OECD countries need FDI capital flows to launch structural transformation from agricultural goods to information technology services. The former offer low economic value, whereas, the latter require high-skill labor and capital investment accumulation in due course. Isard focuses on the important role of FDI capital flows around a review of financial crises in non-OECD countries. These non-OECD countries include Mexico in 1994, Thailand, Indonesia, Malaysia, and South Korea in 1997, and Russia and Brazil in 1998. This analysis ends with the peso problem in Argentina and Turkey in 2001. In the vast majority of these special cases, the IMF offers FDI capital flows in order to safeguard against extreme losses in rare times of financial stress in these non-OECD countries. This case-study evidence therefore targets the broader audience of the global general public.

Isard delves into several economic policy recommendations for IMF-driven reforms worldwide. These policy recommendations specifically target the containment and resolution of financial crises in OECD and non-OECD countries. First, Isard points out the essential need for governments to devise a coherent strategy for financial market liberalization with better exposure to global capital flows. The governments should enhance the provision of financial intermediation services with governance checks and balances in both financial institutions and corporate treasuries. These governments should further adopt flexible exchange rate arrangements. Structural shifts from hard and soft pegs to manageable floats can often help both OECD and non-OECD countries develop significant links to international financial markets. In addition, these governments should strengthen public debt discipline, macro asset market stabilization, and stock market confidence. The governments should open the real economy to foreign finance only after the core regulatory agencies remove serious distortions such as adverse shocks and speculative attacks in the currency markets.

Second, Isard proposes strengthening the quality and impact of IMF surveillance. Some governments should introduce contingent debt contracts for hedging against macroeconomic risks. The governments should address regulatory incentives and distortions that global lenders face in sovereign debt resolution and IMF economic development aid. In terms of financial regulation, these governments should allow most banks to use internal risk models to determine their own minimum regulatory and economic capital requirements. This specific reform focuses on placing higher equity capital requirements on riskier bank credits. In particular, the countercyclical capital buffers help insulate banks from adverse shocks that can arise from regular real business cycle fluctuations. At any rate, the governments should strive to keep the level playing field for local banks and international mega banks. The latter can probably apply complex internal risk models to cause downward pressure on Basel equity capital requirements. This option may or may not be available to local banks in most OECD and non-OECD countries. When push comes to shove, the baseline law of inadvertent consequences counsels caution.

Third, Isard proposes better IMF governance and independence as well as greater non-OECD non-G7 representation at the World Bank and IMF. Also, more radical reforms involve a single world currency, a global lender of last resort, and a global bankruptcy court etc. However, Isard indicates that these radical reforms continue to lack political support even among the G7 governments. The American dollar can continue to be the global reserve currency. The IMF and World Bank both continue to play the dual role of the global lender of last resort. Perhaps it is about time for the G7 governments to convene an international bankruptcy court for better global corporate governance and settlement. Overall, these macrofinancial policy reforms call for greater sovereign state coordination and home-host harmonization.

Nobel Laureate Robert Shiller (2005) refers to several asset bubbles as substantial persistent stock market and residential real estate price hikes. In his classical book Irrational Exuberance, Shiller applies the S&P Case-Shiller Home Price Indices to gauge the extent of excessive house price appreciation across America from 2000 to 2006. In many states and counties, house prices exceed their long-term average equilibrium counterparts by 30% to even 45%. Many banks and non-bank financial institutions extend private credits to home owners via first mortgages, home equity loans, and home equity credit lines. The resultant lax mortgage loan underwriting standards suggest that many mortgage loans turn out to be subprime with poor or low FICO borrower credit scores at higher current loan-to-value (LTV) ratios. As a result, this rare and unique combination eventually leads to massive mortgage loan defaults in America because many borrowers cannot repay the mortgage principal and interest payments. Some of the big banks such as Bear Stearns and Lehman Brothers cannot sustain during such financial turmoil. Credit contagion spreads to many other parts of the world such as Britain, Canada, Europe, Japan, and South East Asia etc. The Global Financial Crisis of 2008-2009 results in substantial stock market price declines as well as a major loss of investor confidence in credit default swaps, corporate debt obligations, and other financial derivative products.

In order to tame animal spirits in asset markets, Nobel Laureates George Akerlof and Robert Shiller (2009) call for greater transparency, better financial disclosure, and new economic measurement made more informative for the general public. In this fundamental sense, investors, shareholders, borrowers, or other stakeholders should be able to decipher core information cascades from complex and esoteric financial reports (such as the Balance Sheets, Income Statements, and Cash Flow Statements). U.S. banks and other financial institutions should make it possible for most borrowers to refinance their residential mortgage loans even when mortgage delinquency rates are on the rise. Most investors should be able to penetrate asset portfolios far enough to make their own financially wise and savvy decisions.

At each step of the information chain, one side knows significantly more than the other about the basic structure of securities. In asset securitization, the bank loan originator often knows more about the actual credit quality of assets (mortgages or home equity credit lines etc), whereas, most investors and borrowers lack this core information. Due to these information asymmetries, most investors can have better confidence in the senior tranche of securities with top Aaa credit grades. As banks transfer basic assets (mortgages, home equity loans, home equity credit lines, and corporate bonds etc) to the special purpose vehicle (SPV), the SPV ensures that the senior tranche of securities can retain top credit quality for only 10% to 15% of the basic assets. The mezzanine and junior equity tranches ultimately lose value when most investors lose confidence in the credit quality of the basic assets. Credit contagion triggers the flight to top credit quality as the mezzanine and junior equity tranches of securities become worthless during the U.S. subprime mortgage crisis and Global Financial Crisis of 2008-2009. When banks originate the basic assets (mortgages, home equity loans, home equity credit lines, and corporate bonds etc) and then distribute various tranches of new securities to both institutional and retail investors, the originate-and-distribute model places blame on the underwriters who foresee no or little exposure to credit concentration risk. Financial trouble can arise from the lax mortgage loan underwriting standards and opaque derivative systems worldwide.

At the same time, bank insolvency fears naturally reduce interbank loans with run-on repo contracts. These fears cause temporary disruptions in the price discovery system of short-term corporate debt markets. A lack of liquidity further exacerbates the Global Financial Crisis. The substantial premium between the mark-to-market values and the actuarial fair values results in a vicious circle of collateral damage. Loose mortgage loan underwriting standards tend to benefit first-time homebuyers who would not otherwise afford to buy residential real estate properties. Numerous home owners who have not defaulted on their mortgage loans become better off. In contrast, those households who have defaulted on their mortgage loans become financially worse off. Some households choose to strategically default on their first mortgages with better access to short-run liquidity through home equity credit lines because it is simply more profitable for these households to do so. As Akerlof and Shiller (2009) suggest in their core thesis, strategic mortgage defaults sometimes reflect animal spirits and self-interests in light of proper economic incentives in the market for lemons (second-hand cars or subprime mortgage loans etc).

Akerlof and Shiller (2009) recommend 2 macro stimulus programs for restoring the economic equilibrium that encompasses the whole U.S. mortgage credit chain. No one has any incentive to rock the boat in equilibrium until residential property prices start to decline dramatically over the short run. First, the proper fiscal and monetary stimulus programs include zero interest rates and the Treasury emergency liquidity provision to the mega banks. The Federal Reserve System, Congress, and Council of Economic Advisers often seem to favor rebuilding the mortgage credit markets over the medium-term pursuit of full employment. Second, the unconventional use of quantitative-easing (QE) large-scale asset purchases (e.g. mortgage securities, credit default swaps, and corporate debt obligations) injects short-term liquidity into the mortgage credit markets. Over several years, the American political economy of both zero interest rates and QE large-scale asset purchases helps achieve the dual mandate of price stability and maximum sustainable employment. In the future, the IMF and World Bank must learn to build macro automatic stabilizers for dealing with the weakest link of credit contagion worldwide. Such automatic stabilizers can help better ring-fence subprime mortgage defaults and other information cascades. In principle, this macro asset market stabilization helps prevent domestic financial crises from triggering global rare disasters in most asset markets.

Harvard macro professors Carmen Reinhart and Kenneth Rogoff (2011) delve into many centuries of financial crises from the Middle Ages to the modern era in global macrofinancial history. The main thesis shows how history can offer not only useful perspective, but also prescient forward guidance in the aftermath. Through this in-depth informative analysis, Reinhart and Rogoff help inspire original empirical work in long-run macrofinancial history. In an empirical view, Reinhart and Rogoff set a higher bar for a comprehensive quantitative historical treatment of financial crises. In contrast to the typical narrative and case-specific methods of financial history by Barry Eichengreen and Charles Kindleberger, Reinhart and Rogoff look for the key general truth that might arise from a panoramic large-sample view. The Reinhart-Rogoff scope of empirical work is very long in terms of time. There is full coverage of pre-1800 macroeconomic events to support the common claim in the book title. After 1800, Reinhart and Rogoff undertake meticulous empirical work to analyze a comprehensive database for 66 countries. The main financial crises include bank, sovereign debt, and currency crises. Reinhart and Rogoff further consider several macrofinancial covariates such as economic output, inflation, exchange rates, and interest rates etc.

From a methodological perspective, the most fundamental and forceful thesis from Reinhart and Rogoff is that global economic history comprises pervasive, episodic, and recurrent sovereign debt, bank, and currency crises in rich and poor countries. These global financial crises are rare events in association with severe economic recessions. From the chambers of power to our academic analysis of global macro financial history, we can learn from the deep Reinhart-Rogoff empirical thesis that substantive cross-country evidence shows rare but episodic crises in the financial system. Reinhart and Rogoff suggest that we can perhaps understand these rare events properly across both space and time. We need to assess the modern macro regimes and institutions in order to better understand dynamic processes at work. In this positive light, Reinhart and Rogoff offer long-term evidence for 66 countries. In this much broader long-run cross-country context, financial crises tend to recur on the basis of common fault lines in the macrofinancial system.

Reinhart and Rogoff provide not only their empirical analysis of global crises in the long run, but also the core policy lessons for fiscal, monetary, and macrofinancial government agencies worldwide. First, some key early warning indicators deserve greater scrutiny. For the ongoing reassessment of macrofinancial conditions, these early warning indicators help identify the optimal trade-offs in monetary and macro financial policies in response to rare disasters on the basis of economic costs and benefits. Recent empirical work includes core composite early warning indicators such as the term spread, the default spread, the S&P 500 P/E ratio, Fama-French fundamental factors for the global stock market, Treasury bond yield curve control, U.S. dollar relative strength index (RSI), Fibonacci retracement, moving average convergence and divergence (MACD), and so on. Some recent empirical evidence suggests that deeper recessions often tend to follow credit booms ceteris paribus. The private-credit-to-GDP ratio proves to be another useful early warning indicator in the broader context of global crises.

Second, supra-national institutions such as the International Monetary Fund (IMF), World Bank, OECD, and Bank for International Settlements (BIS) can collaborate on multilateral solutions and responses to global crises. With enough political clout and power, fiscal and monetary policymakers coordinate their joint efforts to avert rare disasters such as the Global Financial Crisis of 2008-2009 and the pandemic corona virus crisis of 2020-2021. There should be a greater role for the IMF to help advance greater transparency and discipline on most countries before global crisis eruption. Supra-national macro financial cooperation can help a great deal on bank capital, insurance, and short-term liquidity provision with some fiscal form of trans-national support.

Third, global crisis graduation is not easy. Many economists and politicians might have been too naïve to think that their government programs have already solved most macro financial problems and recessions during the U.S. subprime mortgage boom back in 2005-2006. These experts sometimes think that this time is different. However, global economic history shows that numerous sovereign debt, inflation, bank, and currency crises tend to recur at particular historical junctures in both rich and poor countries.

Central bankers often learn to maneuver their monetary policy levers such as zero and negative interest rates, QE large-scale asset purchases, and lax bank reserve requirements. In response to mild financial crises, the central bank often chooses low interest rates in order to boost the real economy and capital accumulation. The central bank can trade foreign dollar reserves in order to help stabilize the currency market through flexible exchange rates. In the Global Financial Crisis of 2008-2009, specifically hitting the zero interest rate and a low 2% inflation target, most central banks such as the Federal Reserve System and European Central Bank soon run out of conventional ammunition. Then these central banks would resort to several unconventional macro large-scale asset purchases in order to restore bank capital and liquidity in the financial system.

Fiscal policymakers often need to introduce countercyclical fiscal deficits and other government expenditures on health care, infrastructure, global trade, finance, and technology in order to bolster the real economy and capital accumulation over time. Across the same trade bloc, some fiscal integration is quite essential for sovereign debt resolution. This fiscal integration can better balance fiscal deficits and inflation risks as the real economy moves from a macro upturn to a severe recession. Fiscal policymakers learn to cap the national debt-to-GDP ratio at some threshold below 90%. This cap helps avoid the negative relation between national debt-to-GDP and real GDP economic growth in global macro history.

Nobel Laureate Joseph Stiglitz (2010) provides his jeremiad and explanation of the freefall pattern in the U.S. subprime mortgage crisis and Global Financial Crisis of 2008-2009. In his prescient view, both economists and politicians cannot separate the subprime mortgage crisis from the earlier dot.com stock market boom and bust. Rather, these financial rare events represent symptoms of a deeper systemic crisis among macro financial institutions such as the Federal Reserve System, European Central Bank, Treasury, IMF, BIS, and World Bank etc. Stiglitz fears that the same worldwide freefall pattern tends to repeat in global economic history. Government half-measures and bad economic policy choices and decisions may inadvertently set up the conditions for an even more severe future financial crisis. In many ways, the polemic tone belies the mainstream nature of the worldwide freefall explanation. Several American, British, and European large banks are too big to fail as national champions in finance. Implicit government guarantees can cause moral hazard in bank credit extension. These fundamental issues require regulatory attention, and the IMF and World Bank learn to launch comprehensive reforms in macrofinance and corporate governance worldwide for better crisis prevention and resolution.

Simon Johnson and James Kwak (2010) contend that the U.S. bank oligarchy is too big to fail as the big banks relentlessly continue to expand their political power and economic influence in Wall Street and Washington. Without structural changes to the macro financial system, America may experience another financial crisis that would be more severe than the Global Financial Crisis of 2008-2009. Johnson and Kwak delve into many decades of U.S. regulatory history that precedes the Global Financial Crisis of 2008-2009. America has a long history of mistrusting big banks. Opponents of big banks include Presidents Thomas Jefferson, Andrew Jackson, Theodore Roosevelt, and Franklin Roosevelt. In the 1970s to 1980s, the U.S. went through significant financial deregulations. Banks were able to transform economic power into political clout in the 1990s. As of early-2010, the top 6 mega banks were U.S. national champions that have become too big to fail in terms of stock market valuation: Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo.

Johnson and Kwak propose a radical policy remedy to prevent the Global Financial Crisis. Breaking up big banks requires Congress to specify limits on bank size, and regulators should strictly enforce these size limits. Johnson and Kwak recommend size limits of about 4% of U.S. GDP for all banks and at least 2% of U.S. GDP for investment banks.

An alternative policy remedy would entail significantly raising capital requirements for big banks or systemically important financial institutions in the macro-prudential stress tests. Nobel Laureate Roger Myerson and Stanford finance professor Anat Admati and their co-authors indicate that the core capital ratio for U.S. large banks should increase to double digits in the reasonable range of 13%-25%. Some recent Federal Reserve research documents empirical evidence in support of this remedy. Either the U.S. regulators break up the big banks to reduce systemic risk exposure, or these regulators should require the mega banks to boost their core capital ratios for better asset market stabilization.

Raghuram Rajan (2010) analyzes the main theme that systematic inequalities tend to create deep financial fault lines and hidden fractures as the root causes of more frequent financial crises worldwide. In America, wealth and income concentration can cause unequal access to higher education and stock market finance. In order to address the political effects of this economic inequality, leaders from both parties have consistently pursued both inclusive institutions and policies to further broaden home ownership through government enterprises such as Fannie Mae and Freddie Mac. Political pressure therefore causes these programs to extend easier credit to less suitable mortgage credit applicants with lower FICO credit scores and higher loan-to-value (LTV) ratios. As a result, such exorbitant mortgage credit expansion culminates in the residential real estate asset bubble and its aftermath in the years from 2005 to 2008. Several other fault lines include the global capital imbalances, the traditionally weak social safety net from health care to infrastructure in America, and the separation of business norms in the financial sector from the best business practices in the real economy.

Rajan proposes a 3-stage attack against the preconditions in support of the Global Financial Crisis of 2008-2009, specifically the subprime mortgage crisis in America. First, Rajan suggests a set of strong social and economic policies for the U.S. state government to reduce inequality with broader educational access and attainment, universal health care, and greater labor mobility across both states and industries. Second, Rajan recommends that international multilateral institutions (such as the IMF and World Bank) build relationships with the constituencies of their component nations. Specifically, the IMF and World Bank should not function just as top-down economic councils of both finance ministers and central bankers. More democratic input and greater transparency should help improve the quality of economic policy choices and decisions made among these international multilateral institutions. In essence, the IMF and World Bank must make fiscal, monetary, and macrofinancial policy recommendations more palatable to their respective member nations. Third, Rajan proposes a complex set of carrots and sticks to defuse the subpar incentives that have accumulated in the American financial sector in recent years. It is about time for the Treasury and Federal Reserve System to remove the implicit promise of government rescue intervention in rare times of severe financial stress (such as the Global Financial Crisis of 2008-2009 and the recent rampant corona virus crisis of 2020-2021). Apart from the dual mandate of general price stability and maximum employment, the government should withdraw state enterprises from the mortgage credit market at a gradual pace in the next decade. Rajan further recommends that the American financial regulators should reconsider the role of deposit insurance. Although deposit insurance has been one of the principal components of American bank regulation, this explicit government guarantee of retail deposits causes moral hazard as many banks strive to extract more economic rent from excessive credit expansion in America and some other parts of the world.

In the meantime, financial corporate governance should reduce the amount of risk that stock market traders prefer to take during an economic boom. Instead of ready and immediate compensation for stock market investment strategies with hidden tail risk, Rajan proposes that a large fraction of executive incentive pay programs should be held in escrow subject to later performance. At the highest levels, boards should choose prudent senior executive managers who take an active interest in shareholder wealth maximization. In effect, these measures can help improve the executive incentive pay pacts in support of better stock market return performance and operational efficiency.

Rajan sees an active role for bank regulators and supervisors. Public transparency and bank supervision would serve as effective checks and balances to hidden tail risk behaviors and best practices in corporate governance. Rajan favors a modern version of the Glass-Steagall Act and some other form of asset segregation. This policy prohibits proprietary traders from investment bank engagements due to the potential abuse of asymmetric information by the banks. To sustain bank solvency, the government should encourage banks to issue long-run convertible bonds; and these bonds convert to equity capital buffers at very specific triggers during some financial crisis. Instead of ad hoc recapitalization during a crisis, bank shareholders bear the costs of open bank recapitalization. Most mega banks should further have clear-cut living wills. In accordance with such ex ante arrangements, the regulators restructure these banks in an efficient and cost-effective manner during the worst-case scenarios.

This analytic essay cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, personal finance tools, and other self-help inspirations. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

We share and circulate these informative posts and essays with hyperlinks through our blogs, podcasts, emails, social media channels, and patent specifications. Our goal is to help promote better financial literacy, inclusion, and freedom of the global general public. While we make a conscious effort to optimize our global reach, this optimization retains our current focus on the American stock market.

This free ebook, AYA Analytica, shares new economic insights, investment memes, and stock portfolio strategies through both blog posts and patent specifications on our AYA fintech network platform. AYA fintech network platform is every investor's social toolkit for profitable investment management. We can help empower stock market investors through technology, education, and social integration.

We hope you enjoy the substantive content of this essay! AYA!

Andy Yeh

Chief Financial Architect (CFA) and Financial Risk Manager (FRM)

Brass Ring International Density Enterprise (BRIDE) ©

Do you find it difficult to beat the long-term average 11% stock market return?

It took us 20+ years to design a new profitable algorithmic asset investment model and its attendant proprietary software technology with fintech patent protection in 2+ years. AYA fintech network platform serves as everyone's first aid for his or her personal stock investment portfolio. Our proprietary software technology allows each investor to leverage fintech intelligence and information without exorbitant time commitment. Our dynamic conditional alpha analysis boosts the typical win rate from 70% to 90%+.

Our new alpha model empowers members to be a wiser stock market investor with profitable alpha signals! The proprietary quantitative analysis applies the collective wisdom of Warren Buffett, George Soros, Carl Icahn, Mark Cuban, Tony Robbins, and Nobel Laureates in finance such as Robert Engle, Eugene Fama, Lars Hansen, Robert Lucas, Robert Merton, Edward Prescott, Thomas Sargent, William Sharpe, Robert Shiller, and Christopher Sims.

Follow our Brass Ring Facebook to learn more about the latest financial news and fantastic stock investment ideas: http://www.facebook.com/brassring2013.

Follow AYA Analytica financial health memo (FHM) podcast channel on YouTube: https://www.youtube.com/channel/UCvntmnacYyCmVyQ-c_qjyyQ

Free signup for stock signals: https://ayafintech.network

Mission on profitable signals: https://ayafintech.network/mission.php

Model technical descriptions: https://ayafintech.network/model.php

Blog on stock alpha signals: https://ayafintech.network/blog.php

Freemium base pricing plans: https://ayafintech.network/freemium.php

Signup for periodic updates: https://ayafintech.network/signup.php

Login for freemium benefits: https://ayafintech.network/login.php

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2023-04-28 16:38:00 Friday ET

Peter Schuck analyzes U.S. government failures and structural problems in light of both institutions and incentives. Peter Schuck (2015) Why

2022-02-22 09:30:00 Tuesday ET

The global asset management industry is central to modern capitalism. Mutual funds, pension funds, sovereign wealth funds, endowment trusts, and asset ma

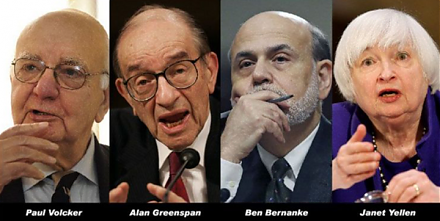

2019-09-23 12:25:00 Monday ET

Volcker, Greenspan, Bernanke, and Yellen contribute to a Wall Street Journal op-ed on monetary policy independence. These former Federal Reserve chiefs unit

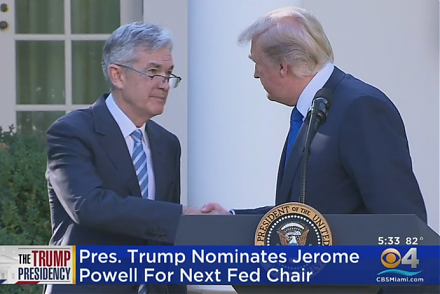

2017-10-03 18:39:00 Tuesday ET

President Trump has nominated Jerome Powell to run the Federal Reserve once Fed Chair Janet Yellen's current term expires in February 2018. Trump's

2018-06-03 07:35:00 Sunday ET

Several recent events explain why Trump may undermine multilateral world order. First, Trump withdraws the U.S. from the 12-nation Trans-Pacific Partnership

2019-09-25 15:33:00 Wednesday ET

Product market competition and online e-commerce help constrain money supply growth with low inflation. Key e-commerce retailers such as Amazon, Alibaba, an