2019-01-02 06:28:00 Wed ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

New York Fed CEO John Williams listens to sharp share price declines as part of the data-dependent interest rate policy. The Federal Reserve can respond to stock market plunges, but key FOMC members still view the U.S. economy as sufficiently strong to grow with higher interest rates. Williams emphasizes softening the central bank language that the next 2 interest rate increases are only economic projections. The upward interest rate trajectory is not a matter of right-or-wrong with Wall Street, and the central bank cannot be on autopilot at this stage of the real business cycle. Williams expects U.S. real GDP to slow to 2%-2.5% in 2019 from 3%-3.5% in 2018, whereas, inflation should be around 2% in 2019. Trump tariffs continue to pose a major tone of economic policy uncertainty.

Treasury Secretary Steven Mnuchin tries to assuage bank CEOs and stock market investors that the Trump administration has no power to oust Fed Chair Jay Powell for his recent interest rate hike. Mnuchin seeks consultation with the Securities and Exchange Commission and Federal Reserve on the partial government shutdown and stock market turmoil. This stock market plunge protection team hence receives reassurance from banks that there is ample liquidity for lending to both consumers and firms.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

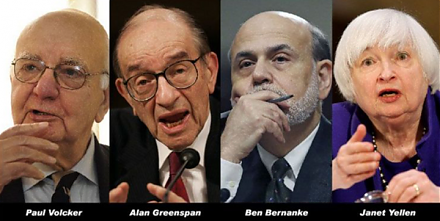

2019-09-23 12:25:00 Monday ET

Volcker, Greenspan, Bernanke, and Yellen contribute to a Wall Street Journal op-ed on monetary policy independence. These former Federal Reserve chiefs unit

2017-02-19 07:41:00 Sunday ET

In his recent book on personal finance, Tony Robbins recommends that each investor should rebalance his or her investment portfolio *only once a year* to in

2017-04-01 06:40:00 Saturday ET

With the current interest rate hike, large banks and insurance companies are likely to benefit from higher equity risk premiums and interest rate spreads.

2018-05-08 13:39:00 Tuesday ET

The Trump administration weighs the pros and cons of a potential mega merger between AT&T and Time Warner. Recent stock prices show favorable trends for

2019-03-19 12:35:00 Tuesday ET

U.S. tech titans increasingly hire PhD economists to help solve business problems. These key tech titans include Facebook, Amazon, Microsoft, Google, Apple,

2023-11-07 11:31:00 Tuesday ET

Joel Mokyr suggests that economic growth arises from a change in cultural beliefs toward technological progress. Joel Mokyr (2018) A culture