2018-02-07 06:38:00 Wed ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

The new Fed chairman Jerome Powell faces a new challenge in the form of both core CPI and CPI inflation rate hikes toward 1.8%-2.1% year-over-year with strong wage growth. The recent greenback depreciation aggravates inflationary concerns as non-farm payroll unemployment declines toward 4% or even 3.9%. This dollar depreciation raises U.S. import prices and therefore can drive greater inflationary momentum. More substantive evidence can shine new light on whether the current Trump stock market rally indicates irrational exuberance for most stock and bond investors.

The Federal Reserve can raise the interest rate to better balance the dual mandate of both price stability and maximum employment. Powell needs to weigh the pros and cons of another interest rate hike that constrains money supply growth near full employment. Price stability helps reduce economic policy uncertainty that may inadvertently dampen both consumption and capital investment decisions. On the other hand, Powell should pick the low-hanging fruits of full employment before America experiences the next gradual deterioration in labor market conditions. During the Trump administration, it takes 3%-3.5% real GDP economic growth for macro momentum to trickle down to the typical U.S. household, firm, and financial intermediary. Supply-side Trumpism needs to prove its feasible case in due course.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2023-01-11 09:26:00 Wednesday ET

Addendum on USPTO fintech patent protection and accreditation As of early-January 2023, the U.S. Patent and Trademark Office (USPTO) has approved our U.S

2019-07-27 17:37:00 Saturday ET

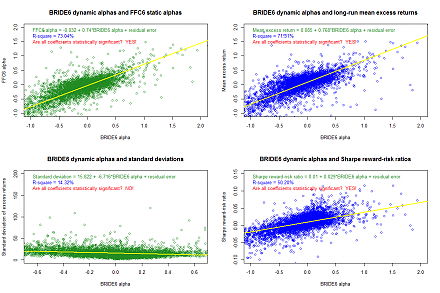

Capital gravitates toward key profitable mutual funds until the marginal asset return equilibrates near the core stock market benchmark. As Stanford finance

2019-11-13 11:34:00 Wednesday ET

The new Brexit deal can boost British pound appreciation and economic optimism. British prime minister Boris Johnson wins the parliamentary vote on his new

2023-09-07 11:30:00 Thursday ET

Michael Woodford provides the theoretical foundations of monetary policy rules in ever more efficient financial markets. Michael Woodford (2003)

2019-08-10 21:44:00 Saturday ET

McKinsey Global Institute analyzes 315 U.S. cities and 3,000 counties in terms of how tech automation affects their workers in the next 5 to 10 years. This

2018-08-17 11:45:00 Friday ET

In accordance with the extant corporate disclosure rules and requirements, all U.S. public corporations have to report their balance sheets, income statemen