2022-04-15 10:32:00 Friday ET

Corporate investment management This review of corporate investment literature focuses on some recent empirical studies of M&A, capital investm

2018-05-23 09:41:00 Wednesday ET

Many U.S. large public corporations spend their tax cuts on new dividend payout and share buyback but not on new job creation and R&D innovation. These

2020-02-05 10:28:00 Wednesday ET

Our proprietary AYA fintech finbuzz essay shines light on the modern collection of business insights with executive annotations and personal reflections. Th

2018-01-08 10:37:00 Monday ET

Spotify considers directly selling its shares to the retail public with no underwriter involvement. The music-streaming company plans a direct list on NYSE

2019-09-23 12:25:00 Monday ET

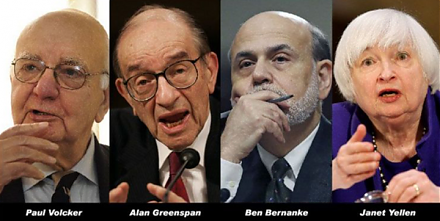

Volcker, Greenspan, Bernanke, and Yellen contribute to a Wall Street Journal op-ed on monetary policy independence. These former Federal Reserve chiefs unit

2025-02-02 11:28:00 Sunday ET

Our proprietary alpha investment model outperforms most stock market indexes from 2017 to 2025. Our proprietary alpha investment model outperforms the ma