Sharpe-Lintner-Black CAPM alpha (Premium Members Only) Fama-French (1993) 3-factor alpha (Premium Members Only) Fama-French-Carhart 4-factor alpha (Premium Members Only) Fama-French (2015) 5-factor alpha (Premium Members Only) Fama-French-Carhart 6-factor alpha (Premium Members Only) Dynamic conditional 6-factor alpha (Premium Members Only) Last update: Saturday 8 August 2026

2019-01-03 10:38:00 Thursday ET

American parents often worry about money and upward mobility for their children. A recent New York Times survey suggests that nowadays American parents spen

2019-02-04 07:42:00 Monday ET

Federal Reserve remains patient on future interest rate adjustments due to global headwinds and impasses over American trade and fiscal budget negotiations.

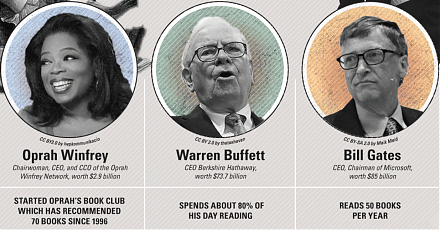

2017-12-17 11:41:00 Sunday ET

Warren Buffett points out that it is important to invest in oneself. Learning about oneself empowers him or her to lead a meaningful life. This valuable inv

2019-11-26 11:30:00 Tuesday ET

AYA Analytica finbuzz podcast channel on YouTube November 2019 In this podcast, we discuss several topical issues as of November 2019: (1) The Trump adm

2019-10-13 16:22:00 Sunday ET

Apple unveils 3 iPhone 11 models with new original video services and stars such as Oprah Winfrey, Jennifer Aniston, and Reese Witherspoon. Apple releases t

2027-01-31 12:25:00 Sunday ET

In recent decades, many governments have chosen to run high fiscal deficits on top of sovereign debt mountains so that greater government intervention still