iShares S&P Asia 50 Index Fund (the Fund) is an exchange-traded fund that seeks investment results that correspond generally to the price and yield performance of the S&P Asia 50 Index (the Index). The Index is a free float-adjusted market capitalization index that is designed to measure the performance of the 50 leading companies from four Asian countries: Hong Kong, South Korea, Singapore and Taiwan. The Fund will concentrate its investments in a particular industry or group of industries to approximately the same extent as the Index is so concentrated. The Fund’s investment advisor is Barclays Global Fund Advisors (BGFA). ...

+See MoreSharpe-Lintner-Black CAPM alpha (Premium Members Only) Fama-French (1993) 3-factor alpha (Premium Members Only) Fama-French-Carhart 4-factor alpha (Premium Members Only) Fama-French (2015) 5-factor alpha (Premium Members Only) Fama-French-Carhart 6-factor alpha (Premium Members Only) Dynamic conditional 6-factor alpha (Premium Members Only) Last update: Saturday 8 August 2026

2017-08-19 14:43:00 Saturday ET

In a recent tweet, President Donald Trump criticizes Amazon over taxes and jobs. Without providing specific evidence, Trump accuses of the e-commerce retail

2022-03-25 09:34:00 Friday ET

Corporate cash management The empirical corporate finance literature suggests four primary motives for firms to hold cash. These motives include the tra

2020-04-03 09:28:00 Friday ET

The Intel trinity of Robert Noyce, Gordon Moore, and Andy Grove establishes the primary semiconductor tech titan in Silicon Valley. Michael Malone (2014)

2018-12-21 11:39:00 Friday ET

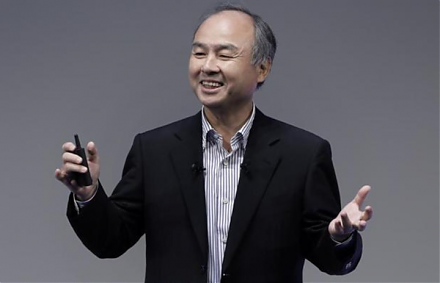

The Internet and telecom conglomerate SoftBank Group raises $23 billion in the biggest IPO in Japan. Going public is part of the major corporate move away f

2018-04-05 07:42:00 Thursday ET

CNBC news anchor Becky Quick interviews Berkshire Hathaway's Warren Buffett in light of the recent stock market gyrations and movements. Warren Buffett

2019-08-04 08:26:00 Sunday ET

U.S. and Chinese trade negotiators hold constructive phone talks after Presidents Trump and Xi exchange reconciliatory gestures at the G20 summit in Japan.