2021-02-02 14:24:00 Tuesday ET

Our proprietary alpha investment model outperforms the major stock market benchmarks such as S&P 500, MSCI, Dow Jones, and Nasdaq. We implement

2025-03-03 04:11:06 Monday ET

Is higher stock market concentration good or bad for Corporate America? In recent years, S&P 500 stock market returns exhibit spectacular concentrati

2027-04-30 12:31:00 Friday ET

In recent years, the current AI-driven stock market rally may or may not turn out to be another major asset bubble in global human history. For the pract

2017-06-21 05:36:00 Wednesday ET

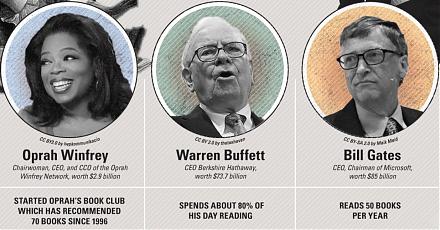

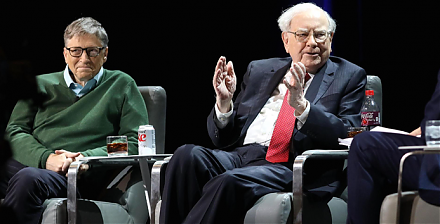

In his latest Berkshire Hathaway annual letter to shareholders, Warren Buffett points out that many people misunderstand his stock investment method in seve

2019-10-21 10:35:00 Monday ET

American state attorneys general begin bipartisan antitrust investigations into the market power and corporate behavior of central tech titans such as Apple

2019-08-07 08:32:00 Wednesday ET

Our fintech finbuzz analytic report shines fresh light on the current global economic outlook. As of Summer-Fall 2019, the current analytic report focuses o