2017-06-15 07:32:00 Thursday ET

President Donald Trump has discussed with the CEOs of large multinational corporations such as Apple, Microsoft, Google, and Amazon. This discussion include

2018-01-17 05:30:00 Wednesday ET

European Union antitrust regulators impose a fine on Qualcomm for advancing its key exclusive microchip deal with Apple to block out rivals such as Intel an

2019-05-07 09:30:00 Tuesday ET

The Trump team receives a 3.2% first-quarter GDP boost as Fed Chair Jay Powell halts the next interest rate hike in early-May 2019. This smooth upward econo

2023-01-09 10:31:00 Monday ET

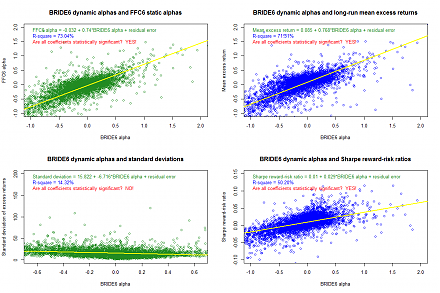

Response to USPTO fintech patent protection As of early-January 2023, the U.S. Patent and Trademark Office (USPTO) has approved our U.S. utility patent

2023-09-14 09:28:00 Thursday ET

Colin Camerer, George Loewenstein, and Matthew Rabin assess the recent advances in the behavioral economic science. Colin Camerer, George Loewenstei

2018-05-23 09:41:00 Wednesday ET

Many U.S. large public corporations spend their tax cuts on new dividend payout and share buyback but not on new job creation and R&D innovation. These