Home > Library > Asset pricing theory and empirical corporate finance

Author Andy Yeh Alpha

This ebook surveys most contemporary topics and issues in modern asset pricing model design and empirical corporate finance. The former focuses on fresh empirical asset pricing tests (e.g. Fama-French factor models), asset pricing models with Epstein-Zin recursive investor preferences, behavioral stock return momentum patterns, and supplementary asset pricing model review notes. The latter delves into many topics in empirical corporate finance such as capital structure, corporate ownership and governance, corporate investment, corporate innovation, net equity issuance, corporate diversification, cash management, corporate payout, and so forth. These surveys and annotations are useful and convenient for the typical graduate student who specializes in modern finance.

macrofinance asset return prediction fama-french capital equity premium puzzle john cochrane corporate finance peter demarzo epstein-zin behavioral finance size value momentum capital structure capital investment corporate ownership and governance corporate innovation cash management corporate payout net equity issuance corporate diversification

Description:

This ebook surveys most contemporary topics and issues in modern asset pricing model design and empirical corporate finance. The former focuses on fresh empirical asset pricing tests (e.g. Fama-French factor models), asset pricing models with Epstein-Zin recursive investor preferences, behavioral stock return momentum patterns, and supplementary asset pricing model review notes. The latter delves into many topics in empirical corporate finance such as capital structure, corporate ownership and governance, corporate investment, corporate innovation, net equity issuance, corporate diversification, cash management, corporate payout, and so forth. These surveys and annotations are useful and convenient for the typical graduate student who specializes in modern finance.

This analytic ebook cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, and other financial issues. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

We share and circulate these informative posts and essays with hyperlinks through our blogs, podcasts, emails, social media channels, and patent specifications. Our goal is to help promote better financial literacy, inclusion, and freedom of the global general public. While we make a conscious effort to optimize our global reach, this optimization retains our current focus on the American stock market.

This ebook shares new economic insights, investment memes, and stock portfolio strategies through both blog posts and patent specifications on our AYA fintech network platform. AYA fintech network platform is every investor's social toolkit for profitable investment management. We can help empower stock market investors through technology, education, and social integration.

2017-12-11 08:42:00 Monday ET

Fed Chair Janet Yellen says the current high stock market valuation does not mean overvaluation. A stock market quick fire sale would pose minimal risk to t

2017-03-09 05:32:00 Thursday ET

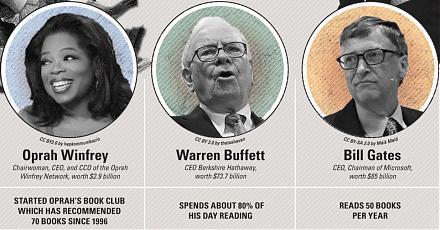

From 1927 to 2017, the U.S. stock market has delivered a hefty average return of about 11% per annum. The U.S. average stock market return is high in stark

2018-03-29 14:28:00 Thursday ET

Share prices tumble for technology stocks due to Trump's criticism of Amazon's tax avoidance, Facebook user data breach of trust, and Tesla autopilo

2025-06-21 10:25:00 Saturday ET

Former New York Times science author and Harvard psychologist Daniel Goleman explains why emotional intelligence can serve as a more important critical succ

2023-04-28 16:38:00 Friday ET

Peter Schuck analyzes U.S. government failures and structural problems in light of both institutions and incentives. Peter Schuck (2015) Why

2023-02-03 08:27:00 Friday ET

Our proprietary alpha investment model outperforms most stock market indices from 2017 to 2023. Our proprietary alpha investment model outperforms the ma