2017-02-19 07:41:00 Sun ET

trust perseverance resilience empathy compassion passion purpose vision mission life metaphors seamless integration critical success factors personal finance entrepreneur inspiration grit

In his recent book on personal finance, Tony Robbins recommends that each investor should rebalance his or her investment portfolio *only once a year* to invest for the long-term.

Robbins defies the conventional wisdom and so suggests that a smart investor should admit that he or she lacks any special advantage in a myopic attempt to beat the market.

A multi-year investment period extends the time horizon for the typical investor to earn both dividend yields and capital gains with much more probable success.

Robbins also points out that it is pivotal for the typical investor to start investing in stocks for their higher long-run average returns during his or her professional career.

Given the power of exponential compound interest growth, dividend yields and capital gains help accumulate capital wealth much faster.

The typical investor's ability to accumulate passive income determines a larger fraction of his or her wealth at retirement age because this income accumulation follows the law of exponential compound interest growth.

In contrast, the typical investor's salaries and bonuses only represent a smaller fraction of his or her wealth at retirement age because this income accumulates over time with no compound interest.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2019-04-30 19:46:00 Tuesday ET

AYA Analytica finbuzz podcast channel on YouTube April 2019 In this podcast, we discuss several topical issues as of April 2019: (1) Our proprietary

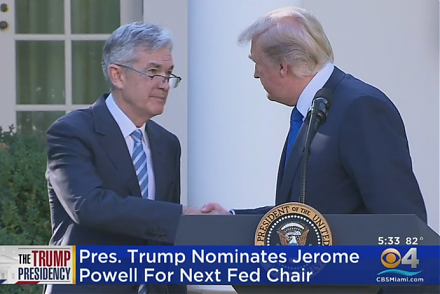

2017-10-03 18:39:00 Tuesday ET

President Trump has nominated Jerome Powell to run the Federal Reserve once Fed Chair Janet Yellen's current term expires in February 2018. Trump's

2023-12-07 07:22:00 Thursday ET

Economic policy incrementalism for better fiscal and monetary policy coordination Traditionally, fiscal and monetary policies were made incrementally. In

2017-02-25 06:44:00 Saturday ET

As the White House economic director, Gary Cohn suggests that the Trump administration will tackle tax cuts after the administration *repeals and replaces*

2021-02-01 10:19:00 Monday ET

In recent times, the International Monetary Fund (IMF) predicts that the fiscal-debt-to-GDP ratio of most rich economies would rise from 95% in 2018 to 135%

2023-11-21 11:32:00 Tuesday ET

Nobel Laureate Paul Milgrom explains the U.S. incentive auction of wireless spectrum allocation from TV broadcasters to telecoms. Paul Milgrom (2019)