2023-05-14 12:31:00 Sun ET

stock market federal reserve monetary policy treasury fiscal policy deficit debt technology covid-19 employment inflation global macro outlook interest rate fiscal stimulus economic growth central bank fomc capital global financial cycle gdp output

Paul Samuelson (1947)

Foundations of economic analysis

In his classic book on Chicago-school economic price theory, Nobel Laureate Paul Anthony Samuelson helps shape the myriad fundamental aspects of the economic science. These aspects include theoretical debates on consumer behavior through economic agent preferences, international trade (the Heckscher-Ohlin-Samuelson model), the traditional Keynesian multiplier-accelerator business cycle model, cost and production theory, dynamic equilibrium systems and comparative statics, and so forth. Foundations of Economic Analysis offers the mathematical concepts and dynamic equilibrium results in Chicago price theory. The Samuelson influence runs through the broader economic science in light of many followers and students such as Nobel Laureates Milton Friedman, Robert Lucas, Robert Merton, Robert Solow, and so forth. With respect to consumption theory, Samuelson suggests that most economic actors reveal their preferences for some bundles of consumption goods by maximizing their life-time utility for a given set of relative price situations. These economic actors improve their economic welfare and lifetime utility on the basis of market observations of individual demand behaviors. The endogenous supply and demand curves intersect to determine the equilibrium market prices and quantities for consumption goods. Economic actors often learn to weigh the trade-offs among the income, wealth, and intertemporal substitution effects of relative price changes in both normal times and rare times of macro financial stress. Empirical evidence shows that most economic actors voluntarily choose to smooth their consumption with permanent income across intertemporal episodes in modern economies.

In the Heckscher-Ohlin-Samuelson model of international trade, there are 2 goods, 2 factors, and 2 countries. Each country operates a free market economy with both consumers and competitive firms. The only point of contact between both countries is trade in goods, and factors cannot move between countries. Each good requires one of the input factors more intensively in the presence of identical technological advances. Under free trade, each country exports the good that uses the abundant factor more intensively in production. This core comparative advantage allows both countries to achieve Pareto efficient improvements in the economic welfare of their residents in terms of life-time economic utility. Moreover, free trade serves as the fundamental force that causes relative factor prices to converge toward their long-term equilibrium time-invariant steady states in both countries. This baseline trade model further applies to the more complex scenario of multiple goods, factors, and countries. This trade model accords with the free market capitalist ideology.

The Hansen-Samuelson multiplier-accelerator model helps analyze the business cycle. The Keynesian multiplier arises as a natural result of both consumption and capital investment accumulation in response to the intermediate rate of economic growth. Samuelson demonstrates that there are several solutions for GDP national income in a standard second-order linear difference equation. At each point in time, GDP national income can be shown as a linear combination of its 1-quarter minus 2-quarter lags. The major parameters reflect the propensity to consume a fraction of GDP national income, as well as the relative pace of capital investment changes in response to changes in aggregate consumption. A high Keynesian multiplier can be indicative of higher economic growth when the government spends more in due course. In accordance with the multiplier-accelerator model, the net positive effect is often greater than the total dollar amount of government expenditures. Whether this Keynesian multiplier can sustain in the long run often depends on fiscal factors such as optimal taxation and public debt issuance.

The cost-of-production theory of value refers to the fact that the price of an object or condition arises from the sum of the costs of available resources in production. The total cost can comprise any of the fundamental factors of production such as capital, labor, land, taxation, and interest etc. Samuelson borrows the Le Chatelier principle from chemistry to analyze the costs of production with multiple factors. In equilibrium, the derivative of the longer-run demand with respect to its own relative price proves to be larger in magnitude than the derivative of the short-term demand ceteris paribus. When the input factors serve as independent variables in the cost function, auxiliary constraints can keep the initial equilibrium state the same in light of a given parameter change. Hence, factor demand and commodity supply curves exhibit lower elasticities in the short run (than demand and supply elasticities in the long run). This equilibrium result arises from the fact that at least some of the total cost remains time-invariant in the short run. In the longer run, firms adjust their mix of input factors such as capital, labor, land, and entrepreneurial innovation etc to better address the variable cost concerns. This economic intuition accords with the Le Chatelier principle.

Samuelson derives and presents the envelope theorem that the long-term average cost curve equates the sum of the short-run average cost curves. Given the primal-dual objective function for consumer utility maximization and cost minimization, the ratio of relative prices reveals the marginal rate of substitution between at least 2 input factors. At the same time, this ratio equates the ratio of marginal utilities for factor usage in cost-effective production. In essence, the representative consumer maximizes his or her life-time utility subject to the cost constraints that each input factor contributes to some part of the total cost (e.g. capital, labor, land, and so on). The representative firm strives to minimize the total cost of production by equating each marginal cost to the respective marginal revenue.

Samuelson formulates the dual value function as the consumer utility function plus the Lagrangian budget cost constraint. As one application of the envelope theorem, the Roy identity states that the Marshallian demand function for the representative consumer is equal to the ratio of partial derivatives of the maximum value function. For instance, we consider the basic case of only 2 input factors in production: labor and capital. Given the optimal values of both factors, the economist first takes the partial derivative of the maximum value function with respect to the optimal wage (i.e. the relative price of labor per unit of time). The economist then takes the partial derivative of the maximum value function with respect to the equilibrium rent or the relative price of capital. The Roy identity shows that the ratio of partial derivatives is equal to the Marshallian demand function for the representative consumer.

In Chicago-school price theory, Samuelson focuses on the mathematical methods for deriving numerical solutions to both linear and non-linear difference equations, determinants, and econometric regressions etc. Samuelson derives and analyzes the second-order conditions for positive definite Hessian matrices (in non-negative quadratic forms). The second-order conditions are quite essential for most optimal solutions to remain within the limits of stability. In many cases, these second-order conditions are sufficient but not necessary in strict mathematical nomenclature. In practice, however, Samuelson suggests that positive definite Hessian matrices are important for most economists to derive the optimal first-order conditions and basic solutions for dynamic asset market stabilization. In the standard asset optimization, the second-order conditions suggest stability and vice versa.

Samuelson uses Fourier series analysis to solve systems of linear equations and determinants. This endeavor empowers Samuelson to find the roots of consumer utility optimization subject to budget cost constraints, Leontief input-output analysis, and the intertemporal elasticity of substitution. This mathematical progress proves to influence the subsequent economic developments in trade, tariff protection, real wage determination, and economic policy evaluation etc. In essence, Samuelson applies mathematical logic to derive operationally meaningful and informative core economic theories. These theories help inform subsequent economic policies and institutions in America and some other parts of the world. The existence of multiple analogies between central features of economic theories often suggests the major existence of more general theories that unify several lemmas with respect to these central features. Samuelson uses this logic to present his cost-of-production theory, consumer utility optimization, international trade, income and wage determination, and business cycle analysis.

Samuelson solves systems of interdependent equilibrium conditions in the Leontief input-output models. The landmark Leontief input-output model serves as a typical quantitative macroeconomic model of interdependencies between different sectors of a given modern economy or different regional economies. The model depicts all inter-industry relations in a modern economy. Moreover, this model shows how the output from one industrial sector can become an input to another industrial sector. In the inter-industry matrix, column entries represent inputs to an industrial sector, whereas, row entries represent outputs from a given sector. This form shows how dependent each sector is on each other sector, both as a customer of outputs from other sectors and as a supplier of inputs to other sectors. Each column of the input-output matrix serves as a vector of the monetary values of inputs to all sectors, so each row represents the monetary value of output from each sector.

Samuelson applies linear algebra to solve the ultimate output vector as the matrix multiplication of an invertible system of linear equations with differential coefficients and the final demand vector. This linear algebra helps gauge total economic output as a result of both inter-industry efficiency gains and final demand quantities. This operation neglects endogenous demand and supply relations. The standard input-output model can often help inform inter-industry trade interactions, environmental carbon emissions, core high-tech clusters, and regional economies etc. In addition to his contribution to the Leontief input-output analysis, Samuelson clarifies several economic concepts such as cardinal utility, independent utility, substitution versus complementarity, and the marginal utility of income or wealth.

Samuelson derives comparative statics (often as partial derivatives with respect to core parameters) to analyze both steady-state properties of solutions and impulse responses in dynamic equilibrium economic systems. In light of these comparative statics and steady-state relations, Samuelson delves into dynamic systems in the fundamental sense that all economic variables can evolve from their arbitrary initial conditions. In this view, Samuelson shows that dynamic equilibrium processes are implicit in modern economic systems. For this reason, it is important for economists to analyze both comparative statics and dynamic responses both over time and in the cross-section.

From a mathematical viewpoint, Samuelson skillfully illustrates some of the various types of math tools from differential and difference equations to integral equations. From currency returns to interest rates, many macroeconomic time series turn out to be random walks. Samuelson refers to the Brownian motion of large molecules as a rich set of random collisions. One of his PhD students, Robert Merton, applies continuous time mathematics (such as the Ito lemma and Feynman-Kac theorem) to derive the canonical price formula for call and put options. This well-known work allows Merton to earn the Nobel Prize in the economic science with Myron Scholes and Fischer Black. Specifically, Merton inherits the Samuelson tradition to derive the Greek letters for option sensitivity analysis. Delta represents the rate of change between the option price and a dollar change in the asset price. Gamma refers to the rate of change between the option delta and the asset price. This second-order price sensitivity indicates the amount of delta movement for each dollar change in the asset price. Theta represents the rate of change in the option price per unit of time. This Greek letter is sometimes known as the time decay (time sensitivity) for a given call or put option. Vega reveals the rate of change between the option price and the conditional volatility of asset returns. Rho reflects the rate of change in the option price for a 1% change in the interest rate. In practice, gamma and vega can approach their respective peaks, and theta approaches its trough, when the asset price approaches the strike price so that the option becomes at-the-money. These key Greek letters and partial derivatives show the comparative statics in derivative option analysis.

Dynamic equilibrium stability analysis is not an esoteric matter that economists can ignore in subsequent research. This stability analysis has become quite important for many economists to figure out dynamic equilibrium first-order and second-order conditions to complement comparative statics. Indeed, the fine distinction between the new classical real business cycle (RBC) theory and the New Keynesian Phillips Curve (NKPC) depends on how fast disequilibrium can revert back to the dynamic equilibrium steady state.

Samuelson applies the correspondence principle to explain the conceptual relation between dynamic equilibrium solutions and comparative statics. Economists often learn to specify the dynamical properties of the economic system in support of the core hypothesis tests for stable equilibrium states or variable movements in motion. This correspondence principle connects the dots between key dynamic equilibrium results and comparative statics as several economists derive definite operationally meaningful economic theories and econometric hypothesis tests. Most economists should study dynamical properties of the economic system in light of steady states and comparative statics. The former shine new light on how disequilibrium persists in motion and then gradually returns to the steady state. The latter often determine the asymptotic equilibrium solutions in the long run. This fundamental distinction is subtle but significant when macro economists refer to long-run monetary neutrality. Short-term disequilibrium departures from the steady state can persist for a while, and the real macroeconomic variables such as economic output, employment, and capital investment accumulation etc converge to their respective steady states. In practice, economic theorems are empirically valid if the data form specific patterns in support of the original hypothesis tests. These stability hypothesis tests have no or little teleological and normative significance.

For Samuelson, the problem with most linear endogenous economic models is that these models cannot explain the random representative amplitude of the business cycle. With a pendulum, the amplitude can be of any magnitude with respect to the initial point of contact. From time to time external exogenous factors come into play. Most economic booms are slow and gradual for several years, and most economic downturns such as the Great Depression of the 1930s and Global Financial Crisis of 2008-2009 are sudden and severe for only a couple of years. This explanation is quite comparable to the rocking horse model of the real business cycle by Nobel Laureate Ragnar Frisch. In accordance with this economic model, a rocking horse hits stochastically with outside shocks to exhibit the usual real business cycle over time. Economic output often moves between full employment and subpar capacity utilization across historical episodes. If the Keynesian multiplier-accelerator model includes some periodic movement such as a sine wave, the dynamic system would settle down to some periodicity due to the exogenous factors such as the oil crisis and the macro financial recession etc (subject to regularity conditions). Samuelson turns to the standard linear deterministic drift plus some Wiener random shock in his deep analysis of each economic time series as a non-linear stochastic dynamic system. The Samuelson applications of both Lagrange multipliers and difference equations etc influence future research on dynamic stochastic general equilibrium (DSGE) macroeconomic models. At this point, it is difficult for most economists to draw a distinction between flexible and sluggish price adjustments in competitive capital markets. This distinction helps inform the different schools of macro thought such as the new classical real business cycle (RBC) theory of monetary neutrality, New Keynesian Phillips Curve (NKPC), and Keynesian search theory in light of an inverse relation between fiscal stimulus and unemployment.

With intricate mathematics, Samuelson connects his PhD thesis book Foundations of Economic Analysis to both the first and second fundamental economic welfare theorems. The first fundamental welfare theorem states that complete markets with complete information and perfect competition can be Pareto optimal in equilibrium. In this sense, no further exchange would make someone better off without making someone else worse off. The baseline requirements for perfect competition include complete information, market power dispersion, and the absence of agency costs, externalities, and information asymmetries. In accordance with the invisible hand metaphor by Adam Smith, competitive markets ensure an efficient allocation of key economic resources. However, there is no guarantee that the single Pareto optimal market outcome is socially desirable. Many possible Pareto efficient allocations of key economic resources can differ in their social desirability with respect to equity and distributive justice.

The second fundamental welfare theorem states that any Pareto optimum serves as a competitive equilibrium for some initial set of endowments. In a positive light, the capitalist exchange economy can support any socially desirable Pareto optimal allocation of key economic resources. On the other hand, some attempts to correct the distribution of major economic resources may introduce distortions via taxation, public debt issuance, and some other social transfer. In this alternative view, it may not be plausible for the modern capitalist exchange economy to attain full optimality with income and wealth re-distribution. Many economists often use the Edgeworth box diagram to help visualize these economic welfare theorems for a simple pure exchange economy.

In his classic book on Chicago-school economic price theory, Nobel Laureate Paul Anthony Samuelson helps shape the myriad fundamental aspects of the economic science. These aspects include theoretical debates on consumer behavior through economic agent preferences, international trade (the Heckscher-Ohlin-Samuelson model), the traditional Keynesian multiplier-accelerator business cycle model, cost and production theory, dynamic equilibrium systems and comparative statics, and so forth. Foundations of Economic Analysis offers the mathematical concepts and dynamic equilibrium results in Chicago price theory. The Samuelson influence runs through the broader economic science in light of many followers and students such as Nobel Laureates Milton Friedman, Robert Lucas, Robert Merton, Robert Solow, and so forth.

This analytic essay cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, personal finance tools, and other self-help inspirations. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

We share and circulate these informative posts and essays with hyperlinks through our blogs, podcasts, emails, social media channels, and patent specifications. Our goal is to help promote better financial literacy, inclusion, and freedom of the global general public. While we make a conscious effort to optimize our global reach, this optimization retains our current focus on the American stock market.

This free ebook, AYA Analytica, shares new economic insights, investment memes, and stock portfolio strategies through both blog posts and patent specifications on our AYA fintech network platform. AYA fintech network platform is every investor's social toolkit for profitable investment management. We can help empower stock market investors through technology, education, and social integration.

We hope you enjoy the substantive content of this essay! AYA!

Andy Yeh

Chief Financial Architect (CFA) and Financial Risk Manager (FRM)

Brass Ring International Density Enterprise (BRIDE) ©

Do you find it difficult to beat the long-term average 11% stock market return?

It took us 20+ years to design a new profitable algorithmic asset investment model and its attendant proprietary software technology with fintech patent protection in 2+ years. AYA fintech network platform serves as everyone's first aid for his or her personal stock investment portfolio. Our proprietary software technology allows each investor to leverage fintech intelligence and information without exorbitant time commitment. Our dynamic conditional alpha analysis boosts the typical win rate from 70% to 90%+.

Our new alpha model empowers members to be a wiser stock market investor with profitable alpha signals! The proprietary quantitative analysis applies the collective wisdom of Warren Buffett, George Soros, Carl Icahn, Mark Cuban, Tony Robbins, and Nobel Laureates in finance such as Robert Engle, Eugene Fama, Lars Hansen, Robert Lucas, Robert Merton, Edward Prescott, Thomas Sargent, William Sharpe, Robert Shiller, and Christopher Sims.

Follow our Brass Ring Facebook to learn more about the latest financial news and fantastic stock investment ideas: http://www.facebook.com/brassring2013.

Follow AYA Analytica financial health memo (FHM) podcast channel on YouTube: https://www.youtube.com/channel/UCvntmnacYyCmVyQ-c_qjyyQ

Free signup for stock signals: https://ayafintech.network

Mission on profitable signals: https://ayafintech.network/mission.php

Model technical descriptions: https://ayafintech.network/model.php

Blog on stock alpha signals: https://ayafintech.network/blog.php

Freemium base pricing plans: https://ayafintech.network/freemium.php

Signup for periodic updates: https://ayafintech.network/signup.php

Login for freemium benefits: https://ayafintech.network/login.ph

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2019-03-15 13:36:00 Friday ET

CNBC stock host Jim Cramer recommends both Caterpillar and Home Depot as the U.S. bull market is likely to continue in light of the recent Fed Chair comment

2022-02-25 00:00:00 Friday ET

Empirical tests of multi-factor models for asset return prediction The capital asset pricing model (CAPM) of Sharpe (1964), Lintner (1965), and Bla

2019-03-13 12:35:00 Wednesday ET

Uber seeks an IPO in close competition with its rideshare rival Lyft and other tech firms such as Slack, Pinterest, and Palantir. Uber expects to complete o

2022-09-15 11:38:00 Thursday ET

Capital structure choices for private firms The Kauffman Firm Survey (KFS) database provides comprehensive panel data on 5,000+ American private firms fr

2017-08-01 09:40:00 Tuesday ET

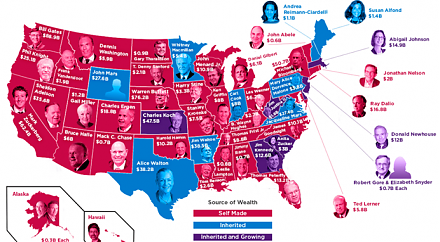

In American states, all of the Top 4 richest people are self-made billionaires: Bill Gates in Washington, Warren Buffett in Nebraska, Michael Bloomberg in N

2025-10-31 12:26:00 Friday ET

With respect to wider weight loss treatment and obesity treatment, the global market for GLP-1 medications now grows substantially to benefit more than 1 bi