2018-04-26 07:37:00 Thu ET

federal reserve monetary policy treasury dollar employment inflation interest rate exchange rate macrofinance recession systemic risk economic growth central bank fomc greenback forward guidance euro capital global financial cycle credit cycle yield curve

Credit supply growth drives business cycle fluctuations and often sows the seeds of their own subsequent destruction. The global financial crisis from 2008 to 2009 suggests that we can predict a key slowdown in real economic activity by tracking incremental household debt accumulation. In both America and 30 other countries, changes in household debt-to-GDP ratios from 2002 to 2007 significantly correlate with increases in unemployment from 2007 to 2010.

From this empirical perspective, credit supply expansions, rather than permanent income or technology shocks, serve as a major driver of real business cycles over time. Most macro models attribute macroeconomic fluctuations to real factors such as exogenous productivity shocks. In contrast, financial intermediaries can play an important role in aggregate credit supply growth, household leverage, employment, and asset valuation. Credit supply expansions affect the real economy by boosting household demand, rather than the productive capacity of firms.

In fact, credit booms tend to precede higher inflation and employment in retail and construction (but not in the tradable or export-driven business sector). The key real economy slowly adjusts to the precipitous decrease in consumer expenditures due to high household leverage when credit supply slows down in major financial crises.

Even when short-term interest rates decline to zero, savers cannot spend enough to make up for the shortfall in aggregate demand. Also, employment cannot readily gravitate from the non-tradable sector to the tradable sector. Key nominal rigidities, sluggish price adjustments, and other legacy distortions render post-credit-boom recessions more severe. What triggers credit supply growth involves a major influx of capital in the financial system.

In this light, both monetary and fiscal stimulus can have a major impact on the real economy via credit supply growth, household debt, stock and bond prices, and real business cycles. Overall, financial stability serves as a core precondition for better bond and stock valuation.

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2019-04-09 11:29:00 Tuesday ET

The U.S. Treasury yield curve inverts for the first time since the Global Financial Crisis. The key term spread between the 10-year and 3-month U.S. Treasur

2019-04-23 19:45:00 Tuesday ET

Income and wealth concentration follows the ebbs and flows of the business cycle in America. Economic inequality not only grows among people, but it also gr

2017-12-14 12:41:00 Thursday ET

Federal Reserve raises the interest rate by 25 basis points to the target range of 1.25% to 1.5% as FOMC members revise up their GDP estimate from 2% to 2.5

2023-02-28 10:27:00 Tuesday ET

Basic income reforms can contribute to better health care, public infrastructure, education, technology, and residential protection. Philippe Van Parijs

2019-08-31 14:39:00 Saturday ET

AYA Analytica finbuzz podcast channel on YouTube August 2019 In this podcast, we discuss several topical issues as of August 2019: (1) Warren B

2019-04-27 16:41:00 Saturday ET

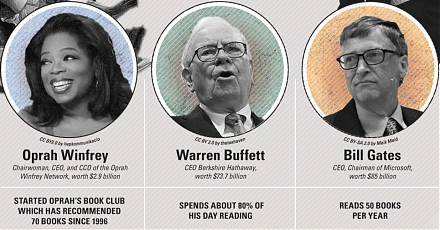

Tony Robbins suggests that one has to be able to make money during sleep hours in order to reach financial freedom. Most of our jobs and life experiences tr