2020-02-05 10:28:00 Wednesday ET

Our proprietary AYA fintech finbuzz essay shines light on the modern collection of business insights with executive annotations and personal reflections. Th

2019-02-03 13:39:00 Sunday ET

It can be practical for the U.S. to impose the 2% wealth tax on the rich. Democratic Senator Elizabeth Warren proposes a 2% wealth tax on the richest Americ

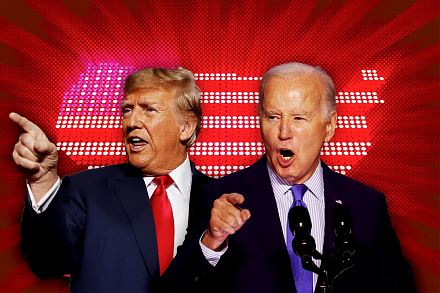

2024-03-19 03:35:58 Tuesday ET

U.S. presidential election: a re-match between Biden and Trump in November 2024 We delve into the 5 major economic themes of the U.S. presidential electi

2019-05-15 12:32:00 Wednesday ET

The May administration needs to seek a fresh fallback option for Halloween Brexit. After the House of Commons rejects Brexit proposals from the May administ

2018-04-05 07:42:00 Thursday ET

CNBC news anchor Becky Quick interviews Berkshire Hathaway's Warren Buffett in light of the recent stock market gyrations and movements. Warren Buffett

2019-07-07 18:36:00 Sunday ET

The Chinese central bank has to circumvent offshore imports-driven inflation due to Renminbi currency misalignment. Even though China keeps substantial fore