2020-09-15 08:38:00 Tue ET

stock market federal reserve monetary policy covid-19 alpha interest rate macrofinance global economic outlook volatility economic policy uncertainty recession eigenvalue stock return s&p 500 covariance matrix value momentum fiscal stimulus global financial crisis rational risk behavioral finance

Macro eigenvalue volatility helps predict some recent episodes of high economic policy uncertainty, recession risk, or rare events such as the recent rampant global corona virus pandemic outbreak.

September 2020

We perform principal component analysis of S&P 500 daily stock returns in the most recent time frame from January 2015 to September 2020. We focus on the daily data span with 4-year time window slides over time, so the first 4-year time window from January 2015 to December 2018 rolls over day-by-day to the present. This empirical analysis helps gauge both macro financial conditions and fundamental economic relations over time. Stock market beliefs can help inform both fiscal and monetary reactions for the U.S. Treasury and Federal Reserve to achieve maximum sustainable employment, robust economic growth, price stability, and asset market stabilization.

We assess whether the large S&P 500 stock return eigenvalues exhibit greater variability over time. This quantitative assessment shines fresh light on the principal component analysis of asset returns in the broader context of macro market stabilization. The resultant analysis helps inform algorithmic regularization in most quantitative fundamental factor models.

The empirical results show that the first 10 principal components explain almost 60% of variance in the covariance matrix of S&P 500 daily stock returns. The first principal component explains 42.2% of variance in the covariance matrix; the second principal component explains 5.0% of variance in the covariance matrix; and the third principal component explains 3.5% of variance in the covariance matrix (and so forth).

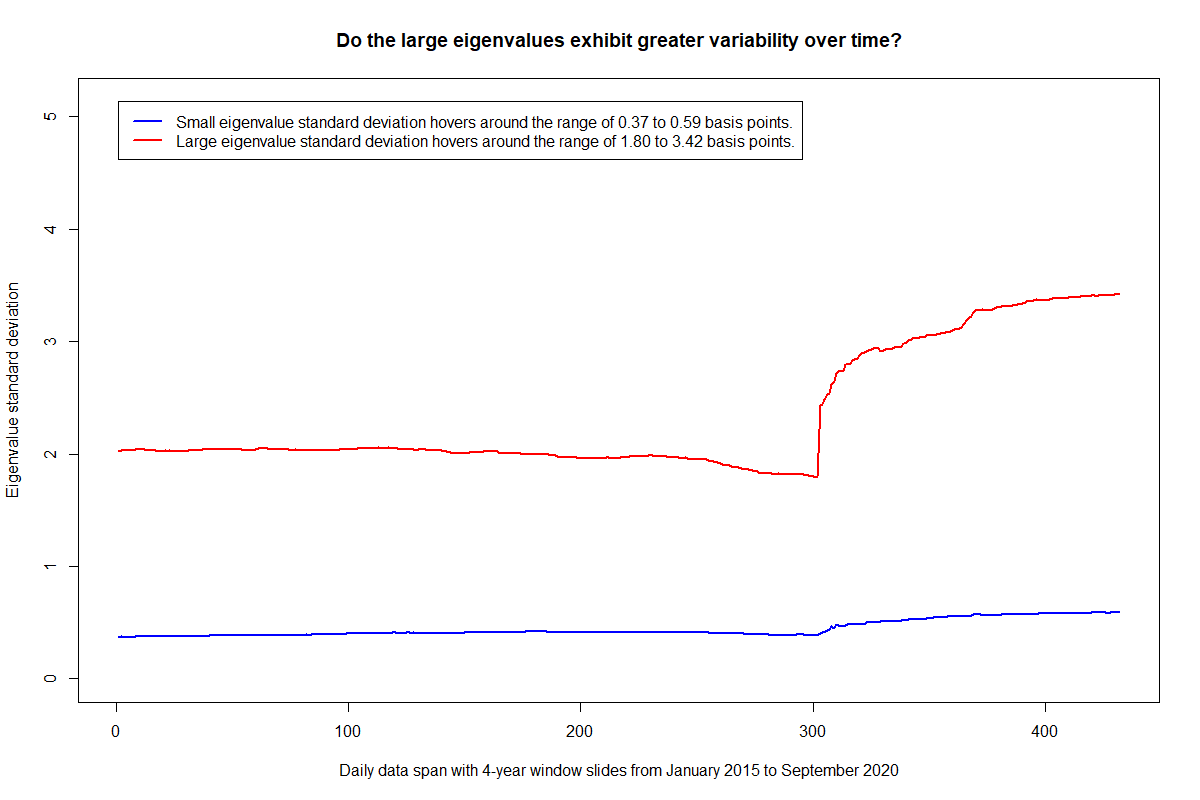

We want to assess whether the high S&P 500 stock return eigenvalues exhibit greater variability over time in response to rare episodes of high economic policy uncertainty, recession risk, or exogenous Covid-19 airborne transmission. We compute the standard deviation (or real volatility) of S&P 500 stock return eigenvalues in the cross-section at daily frequency. This computation applies to both the small and large eigenvalues respectively. We can choose to use the coefficient of variation (or the ratio of eigenvalue standard deviation to its mean) as an alternative measure of eigenvalue variation. The same qualitative conclusion remains robust in either case.

The standard deviation of small eigenvalues hovers around the range of 0.37 basis points to 0.59 basis points, whereas, the standard deviation of large eigenvalues hovers around the range of 1.80 basis points to 3.42 basis points. As shown in the time-series plot of S&P 500 eigenvalue volatility from January 2015 to September 2020, the sudden subsequent spike in S&P 500 eigenvalue volatility arises from the recent rampant global corona virus pandemic outbreak. This evidence shows that the large S&P 500 stock return eigenvalues tend to exhibit greater variability in response to Covid-19 over time. At the same time, the smaller eigenvalues cannot fluctuate enough to pick up this macro trend. For this reason, the small eigenvalues may be inadvertently subject to idiosyncratic risk. In this new light, the small eigenvalues tend to contain too much noise with virtually no or little response to macroeconomic structural shifts and megatrends.

Algorithmic regularization helps impose reasonable penalties on both small and large eigenvalues in most quantitative fundamental factor models. These models help us discover the informative relations between fundamental factors and macroeconomic innovations. Given the evidence, this experiment affirms the economic intuition that the large S&P 500 stock return eigenvalues fluctuate substantially to reflect the generic stock market decline right after the recent rampant global corona virus pandemic outbreak.

We can generalize this empirical analysis to establish casual relations between macro eigenvalue volatility and several fundamental time-series indicators of financial market strength. In particular, we can apply macro eigenvalue volatility to delve into the relative likelihood of economic recession risk in accordance with the trademark NBER definition. Also, we can use macro eigenvalue volatility to help explain the first few moment conditions for the equity premium puzzle and asset market anomaly persistence. Moreover, we can use macro eigenvalue volatility to help gauge both typical and special macro financial conditions. This practical application can contribute to the regulatory requirements for higher financial intermediary capital for most banks and insurers etc to better absorb extreme losses that may arise from rare times of severe financial stress (such as the Global Financial Crisis of 2008-2009, European sovereign debt debacle, and Covid-19-driven asset market dynamism). We can further use macro eigenvalue volatility to help predict some recent episodes of substantially higher economic policy uncertainty. This latter prediction can be specifically useful in light of the recent rare $4 trillion fiscal and monetary stimulus from the Trump administration.

Our quantitative assessment further helps inform the canonical Taylor interest rate rules. Most macro economists fixate on the appropriate interest rate response to price inflation, wage inflation, and economic output etc, whereas, the current empirical analysis suggests the vital and essential need for asset market stabilization. From time to time, the monetary authority has to institute commensurate dovish central bank decisions to complement fiscal stimulus to safeguard against severe macro financial stress in rare events such as the recent rampant global corona virus pandemic outbreak and the Global Financial Crisis of 2008-2009.

In fact, the neoclassic school of macroeconomic thought suggests that the welfare cost of inflation is quite low or no more than 0.1% to 0.3% of total real GDP per annum. Also, Keynesian search theory indicates that the steady-state unemployment rate is often indeterminate as a result of labor market frictions. In this fresh light, the self-fulfilling beliefs of stock market valuation can often help inform the long prevalent unemployment rate in equilibrium. In a unique fashion, the New Keynesian Phillips Curve has substantially flattened since the Great Moderation of both low inflation and low economic growth (or secular stagnation) around the turn of the new century. Since the mid-1990s, we have seen virtually no mysterious and inexorable trade-off between inflation and unemployment. In a nutshell, both the U.S. Treasury and Federal Reserve must coordinate their rare fiscal and monetary stimulus to sustain most macro financial markets for stocks, bonds, currencies, and commodities etc at this particular juncture of global economic history.

Our empirical analysis demonstrates that macro eigenvalue volatility helps predict some recent episodes of high economic policy uncertainty, recession risk, or rare events such as the recent rampant global corona virus pandemic outbreak. This analysis helps gauge both macro financial conditions and economic relations over time. Stock market beliefs can help inform both fiscal and monetary reactions for both the U.S. Treasury and Federal Reserve to achieve maximum sustainable employment, robust economic growth, price stability, and asset market stabilization.

There is an informative, persistent, and econometrically significant negative relation between the long-short decile return spreads for value and momentum. Neither the q-theoretic rational risk models nor the behavioral mispricing models can explain this pervasive empirical phenomenon. In fact, this empirical phenomenon prevails not only in the U.S. stock market but also in the major global markets for stocks, bonds, currencies, and commodities etc.

Professional arbitrageurs can perhaps decipher value portfolio returns to help better improve momentum portfolio returns and vice versa. Dynamic conditional factor premiums often exhibit mutual causation with macroeconomic surprises and innovations. This causation can hence serve as a core qualifying condition for fundamental factor selection. To the extent that macro financial fluctuations manifest in the form of average asset return gyrations, these causal linkages help us better demystify the long prevalent puzzle of an empirically robust trade-off between value and momentum.

This analytic essay cannot constitute any form of financial advice, analyst opinion, recommendation, or endorsement. We refrain from engaging in financial advisory services, and we seek to offer our analytic insights into the latest economic trends, stock market topics, investment memes, personal finance tools, and other self-help inspirations. Our proprietary alpha investment algorithmic system helps enrich our AYA fintech network platform as a new social community for stock market investors: https://ayafintech.network.

We share and circulate these informative posts and essays with hyperlinks through our blogs, podcasts, emails, social media channels, and patent specifications. Our goal is to help promote better financial literacy, inclusion, and freedom of the global general public. While we make a conscious effort to optimize our global reach, this optimization retains our current focus on the American stock market.

This free ebook, AYA Analytica, shares new economic insights, investment memes, and stock portfolio strategies through both blog posts and patent specifications on our AYA fintech network platform. AYA fintech network platform is every investor's social toolkit for profitable investment management. We can help empower stock market investors through technology, education, and social integration.

We hope you enjoy the substantive content of this essay! AYA!

Andy Yeh

Chief Financial Architect (CFA) and Financial Risk Manager (FRM)

Brass Ring International Density Enterprise (BRIDE) ©

Do you find it difficult to beat the long-term average 11% stock market return?

It took us 20+ years to design a new profitable algorithmic asset investment model and its attendant proprietary software technology with fintech patent protection in 2+ years. AYA fintech network platform serves as everyone's first aid for his or her personal stock investment portfolio. Our proprietary software technology allows each investor to leverage fintech intelligence and information without exorbitant time commitment. Our dynamic conditional alpha analysis boosts the typical win rate from 70% to 90%+.

Our new alpha model empowers members to be a wiser stock market investor with profitable alpha signals! The proprietary quantitative analysis applies the collective wisdom of Warren Buffett, George Soros, Carl Icahn, Mark Cuban, Tony Robbins, and Nobel Laureates in finance such as Robert Engle, Eugene Fama, Lars Hansen, Robert Lucas, Robert Merton, Edward Prescott, Thomas Sargent, William Sharpe, Robert Shiller, and Christopher Sims.

Follow AYA Analytica financial health memo (FHM) podcast channel on YouTube: https://www.youtube.com/channel/UCvntmnacYyCmVyQ-c_qjyyQ

Follow our Brass Ring Facebook to learn more about the latest financial news and fantastic stock investment ideas: http://www.facebook.com/brassring2013.

Free signup for stock signals: https://ayafintech.network

Mission on profitable signals: https://ayafintech.network/mission.php

Model technical descriptions: https://ayafintech.network/model.php

Blog on stock alpha signals: https://ayafintech.network/blog.php

Freemium base pricing plans: https://ayafintech.network/freemium.php

Signup for periodic updates: https://ayafintech.network/signup.php

Login for freemium benefits: https://ayafintech.network/login.php

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2018-06-25 12:43:00 Monday ET

Apple and Samsung are the archrivals for the title of the world's top smart phone maker. The recent patent lawsuit settlement between Apple and Samsung

2019-10-21 10:35:00 Monday ET

American state attorneys general begin bipartisan antitrust investigations into the market power and corporate behavior of central tech titans such as Apple

2018-02-27 09:35:00 Tuesday ET

Fed's new chairman Jerome Powell testifies before Congress for the first time. He vows to prevent price instability for U.S. consumers, firms, and finan

2016-10-01 00:00:00 Saturday ET

We can learn much from the frugal habits and lifestyles of several billionaires on earth. Warren Buffett, Chairman and CEO of Berkshire Hathaway, still l

2018-04-11 09:37:00 Wednesday ET

North Korean leader and president Kim Jong-Un seeks peaceful resolution and denuclearization on the Korean Peninsula. When *peace* comes to shove, Asia

2019-08-31 14:39:00 Saturday ET

AYA Analytica finbuzz podcast channel on YouTube August 2019 In this podcast, we discuss several topical issues as of August 2019: (1) Warren B