Ferrari N.V. is engaged in designing, manufacturing and selling sports cars. Its products include sports car models consists of 458 Italia, 488 GTB, 458 Spider, 488 Spider, F12 Berlinetta, 458 Speciale and 458 Speciale A as well as two grand tourer (GT) cars: California T and FF. The Company also produces a limited edition supercar, LaFerrari and limited series and one-off cars. It operates primarily in Europe, the Middle East, India, Africa, Americas, Greater China and Rest of Asia-Pacific region. Ferrari N.V. is headquartered in Maranello, Italy....

+See MoreSharpe-Lintner-Black CAPM alpha (Premium Members Only) Fama-French (1993) 3-factor alpha (Premium Members Only) Fama-French-Carhart 4-factor alpha (Premium Members Only) Fama-French (2015) 5-factor alpha (Premium Members Only) Fama-French-Carhart 6-factor alpha (Premium Members Only) Dynamic conditional 6-factor alpha (Premium Members Only) Last update: Saturday 8 August 2026

2025-10-08 11:34:00 Wednesday ET

Stock Synopsis: With a new Python program, we use, adapt, apply, and leverage each of the mainstream Gemini Gen AI models to conduct this comprehensive fund

2020-09-17 12:28:00 Thursday ET

Many successful business organizations develop their distinctive capabilities and unique value propositions for strategic reasons. Paul Leinwand and Cesa

2023-12-03 11:33:00 Sunday ET

Macro innovations and asset alphas show significant mutual causation. April 2023 This brief article draws from the recent research publicati

2019-12-16 11:37:00 Monday ET

America and China cannot decouple decades of long-term collaboration in trade, finance, and technology. In recent times, some economists claim that China ma

2019-09-23 12:25:00 Monday ET

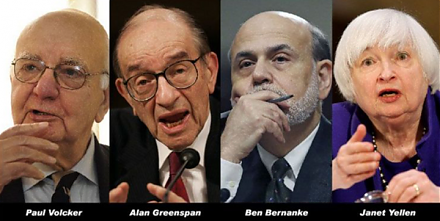

Volcker, Greenspan, Bernanke, and Yellen contribute to a Wall Street Journal op-ed on monetary policy independence. These former Federal Reserve chiefs unit

2019-09-03 14:29:00 Tuesday ET

Due to U.S. tariffs and other cloudy causes of economic policy uncertainty, Apple, Nintendo, and Samsung start to consider making tech products in Vietnam i