2019-07-29 11:33:00 Mon ET

stock market competition macrofinance stock return s&p 500 financial crisis financial deregulation bank oligarchy systemic risk asset market stabilization asset price fluctuations regulation capital financial stability dodd-frank

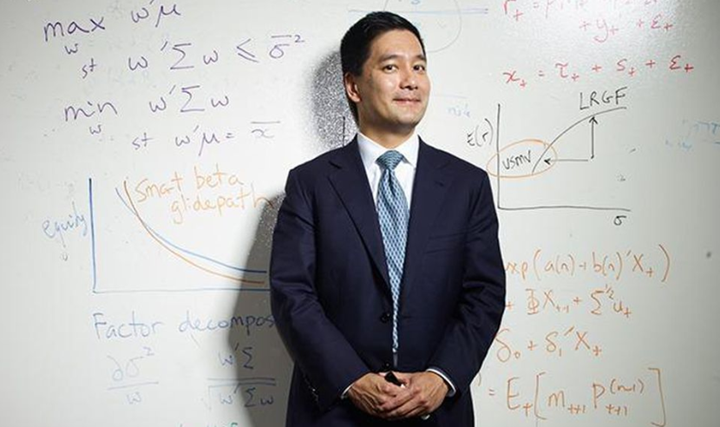

Blackrock asset research director Andrew Ang shares his economic insights into fundamental factors for global asset management. As Ang indicates in an interview with Ritholtz Wealth Management, fundamental factor investors seek to manage macroeconomic risk to enhance their average returns. Ang focuses on 5 primary factors: size, value, momentum, low volatility, and high quality of profit margins. In addition, Ang oversees a broad basket of assets such as stocks, bonds, currencies, and commodities.

The consistent application of both big data and technology helps scale total assets under management with lower transaction costs. At BlackRock, Ang decomposes his favorite fundamental factors across macro and style factors. The 3 major macro factors are *economic growth, inflation, and the real interest rate*, in accordance with the baseline Taylor interest rate that depicts a highly non-linear Phillips curve. Ang empirically finds that these 3 macroeconomic factors account for 85% of stock market returns. Stock portfolio analysis helps achieve higher average returns (after risk and fee adjustments) when the active fund manager focuses on size, value, momentum, low volatility, and corporate profitability. Moreover, value occasionally becomes more cost-effective relative to its own history, and key momentum returns often cluster together in specific time periods. This factor investment methodology accords with our proprietary alpha investment model that relies on 6 fundamental factors (size, value, momentum, asset growth, operating profitability, and market risk exposure).

If any of our AYA Analytica financial health memos (FHM), blog posts, ebooks, newsletters, and notifications etc, or any other form of online content curation, involves potential copyright concerns, please feel free to contact us at service@ayafintech.network so that we can remove relevant content in response to any such request within a reasonable time frame.

2019-01-07 18:42:00 Monday ET

Neoliberal public choice continues to spin national taxation and several other forms of government intervention. The key post-crisis consensus focuses on go

2026-07-01 11:29:00 Wednesday ET

In recent years, higher American economic growth has been impressive both by historical standards and in comparison to the rest of the world. American excep

2024-04-02 04:45:41 Tuesday ET

Stock Synopsis: High-speed 5G broadband and mobile cloud telecommunication In the U.S. telecom industry for high-speed Internet connections and mobile cl

2022-10-25 11:31:00 Tuesday ET

Corporate investment insights from mergers and acquisitions Relative market misvaluation between the bidder and target firms drives most waves of mergers

2019-12-22 08:30:00 Sunday ET

European Commission President Ursula von der Leyen now protects the European circular economy and green growth from 2020 to 2050. The new circular economy r

2019-08-01 11:33:00 Thursday ET

Many young and mid-career Americans fall into the financial distress trap in rural communities. A recent analysis of 25,800 zip codes for 99% of the U.S. po